Question

2. Calculate the rate of return on a price-weighted index of the three stocks for the period (t = 0 to t = 1). 3.

2. Calculate the rate of return on a price-weighted index of the three stocks for the period (t = 0 to t = 1).

3. If the index is a market value-weighted index and the market value-weighted index was 218 at t=0, what is the new index value at t=1?

4. If the index is an equal-weighted index and the equal-weighted index was 218 at t=0, what is the new index value at t=1?

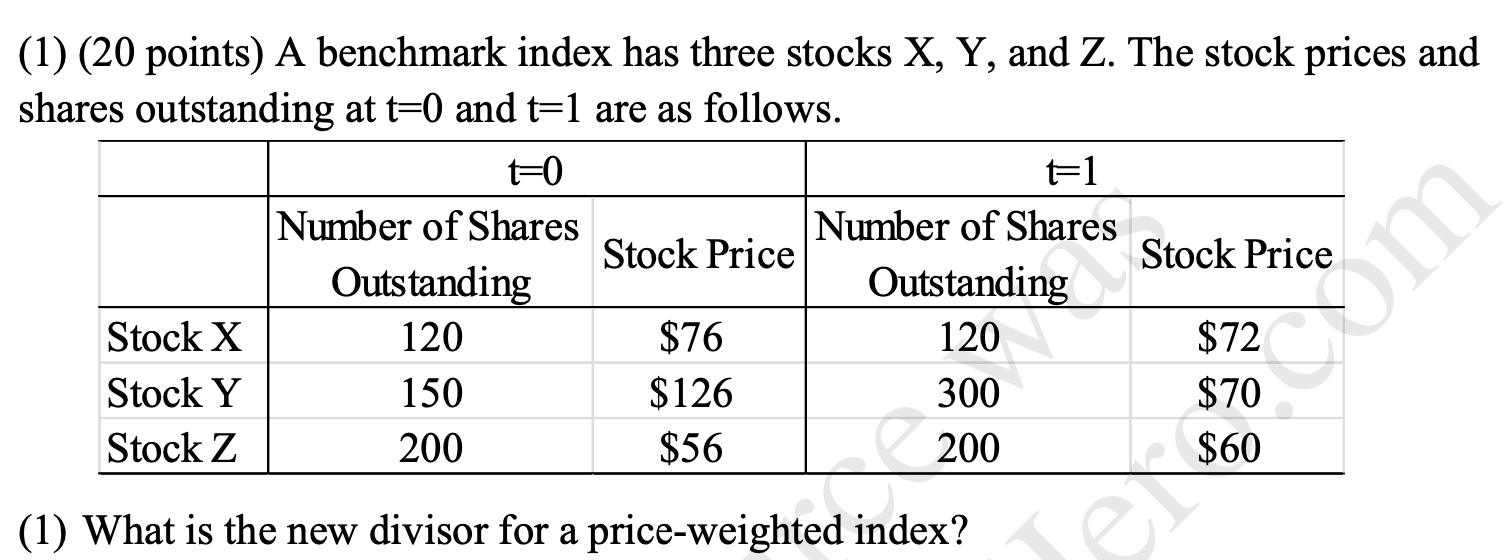

(1) (20 points) A benchmark index has three stocks X, Y, and Z. The stock prices and shares outstanding at t=0 and t=1 are as follows. to F1 Number of Shares Number of Shares Stock Price Stock Price Outstanding Outstanding Stock X 120 $76 120 $72 Stock Y 150 $126 300 $70 Stock Z 200 $56 $60 200 (1) What is the new divisor for a price-weighted index? (1) (20 points) A benchmark index has three stocks X, Y, and Z. The stock prices and shares outstanding at t=0 and t=1 are as follows. to F1 Number of Shares Number of Shares Stock Price Stock Price Outstanding Outstanding Stock X 120 $76 120 $72 Stock Y 150 $126 300 $70 Stock Z 200 $56 $60 200 (1) What is the new divisor for a price-weighted indexStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of The Economics Of Finance Corporate Finance Volume 1A

Authors: George M. Constantinides, M. Harris, Rene M. Stulz

1st Edition

0444513620, 978-0444513625