Answered step by step

Verified Expert Solution

Question

1 Approved Answer

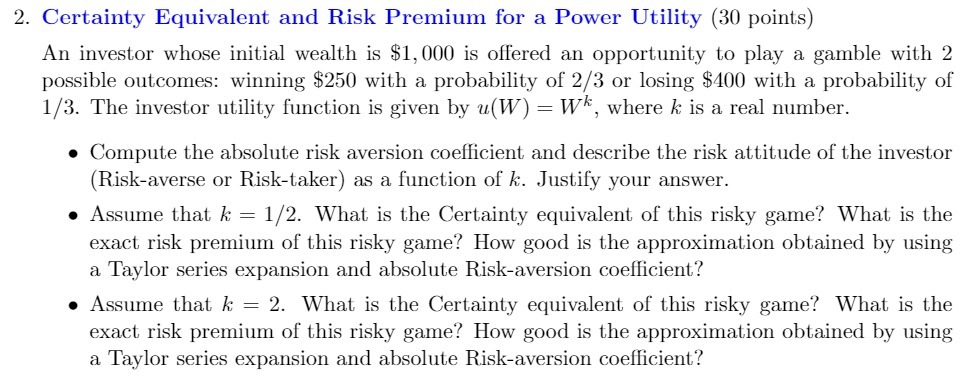

2. Certainty Equivalent and Risk Premium for a Power Utility (30 points) An investor whose initial wealth is $1,000 is offered an opportunity to

2. Certainty Equivalent and Risk Premium for a Power Utility (30 points) An investor whose initial wealth is $1,000 is offered an opportunity to play a gamble with 2 possible outcomes: winning $250 with a probability of 2/3 or losing $400 with a probability of 1/3. The investor utility function is given by u(W) = Wk, where k is a real number. Compute the absolute risk aversion coefficient and describe the risk attitude of the investor (Risk-averse or Risk-taker) as a function of k. Justify your answer. Assume that k = 1/2. What is the Certainty equivalent of this risky game? What is the exact risk premium of this risky game? How good is the approximation obtained by using a Taylor series expansion and absolute Risk-aversion coefficient? Assume that k = 2. What is the Certainty equivalent of this risky game? What is the exact risk premium of this risky game? How good is the approximation obtained by using a Taylor series expansion and absolute Risk-aversion coefficient?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To compute the absolute risk aversion coefficient and analyze the risk attitude of the investor well first calculate the expected utility and then der...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agricultural Finance

Authors: Charles Moss

1st Edition

0415599075, 978-0415599078