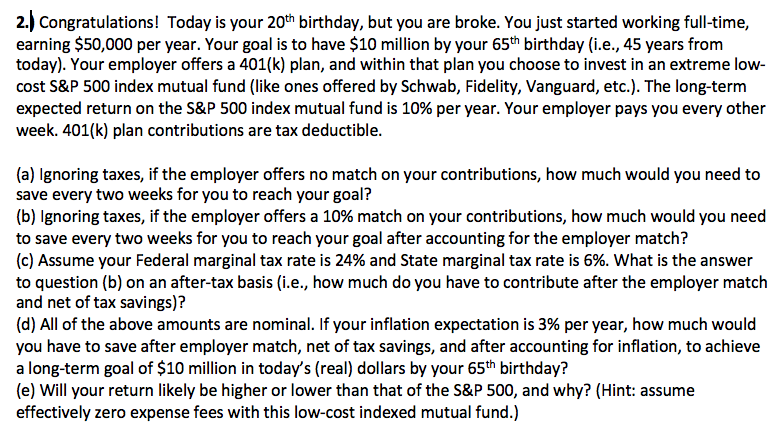

2.) Congratulations! Today is your 20th birthday, but you are broke. You just started working full-time, earning $50,000 per year. Your goal is to have $10 million by your 65th birthday (i.e., 45 years from today). Your employer offers a 401(k) plan, and within that plan you choose to invest in an extreme low- cost S&P 500 index mutual fund (like ones offered by Schwab, Fidelity, Vanguard, etc.). The long-term expected return on the S&P 500 index mutual fund is 10% per year. Your employer pays you every other week. 401(k) plan contributions are tax deductible (a) lgnoring taxes, if the employer offers no match on your contributions, how much would you need to save every two weeks for you to reach your goal? (b) Ignoring taxes, if the employer offers a 10% match on your contributions, how much would you need to save every two weeks for you to reach your goal after accounting for the employer match? (c) Assume your Federal marginal tax rate is 24% and State marginal tax rate is 6%. what is the answer to question (b) on an after-tax basis (i.e., how much do you have to contribute after the employer match and net of tax savings)? (d) All of the above amounts are nominal. If your inflation expectation is 3% per year, how much would you have to save after employer match, net of tax savings, and after accounting for inflation, to achieve a long-term goal of $10 million in today's (real) dollars by your 65th birthday? (e) Will your return likely be higher or lower than that of the S&P 500, and why? (Hint: assume effectively zero expense fees with this low-cost indexed mutual fund.) 2.) Congratulations! Today is your 20th birthday, but you are broke. You just started working full-time, earning $50,000 per year. Your goal is to have $10 million by your 65th birthday (i.e., 45 years from today). Your employer offers a 401(k) plan, and within that plan you choose to invest in an extreme low- cost S&P 500 index mutual fund (like ones offered by Schwab, Fidelity, Vanguard, etc.). The long-term expected return on the S&P 500 index mutual fund is 10% per year. Your employer pays you every other week. 401(k) plan contributions are tax deductible (a) lgnoring taxes, if the employer offers no match on your contributions, how much would you need to save every two weeks for you to reach your goal? (b) Ignoring taxes, if the employer offers a 10% match on your contributions, how much would you need to save every two weeks for you to reach your goal after accounting for the employer match? (c) Assume your Federal marginal tax rate is 24% and State marginal tax rate is 6%. what is the answer to question (b) on an after-tax basis (i.e., how much do you have to contribute after the employer match and net of tax savings)? (d) All of the above amounts are nominal. If your inflation expectation is 3% per year, how much would you have to save after employer match, net of tax savings, and after accounting for inflation, to achieve a long-term goal of $10 million in today's (real) dollars by your 65th birthday? (e) Will your return likely be higher or lower than that of the S&P 500, and why? (Hint: assume effectively zero expense fees with this low-cost indexed mutual fund.)