Question

2) Construct a binomial interest rate tree assuming conditions (i)-(v): i) the constant annual volatility of 10%, ii) probabilities for each movement are 50%, iii)

2) Construct a binomial interest rate tree assuming conditions (i)-(v): i) the constant annual volatility of 10%, ii) probabilities for each movement are 50%, iii) the log of the rate when the price goes down is one standard deviation down from the mean 1-year forward rate starting at each corresponding year, iv) the log of the rate when the price goes up is one standard deviation up from the mean 1-year forward rate starting at each corresponding year, v) the interest rates should match the forward rates. 3) Consider a bond with three months to maturity and a monthly coupon rate of 2%. Use the binomial tree above to price this bond.

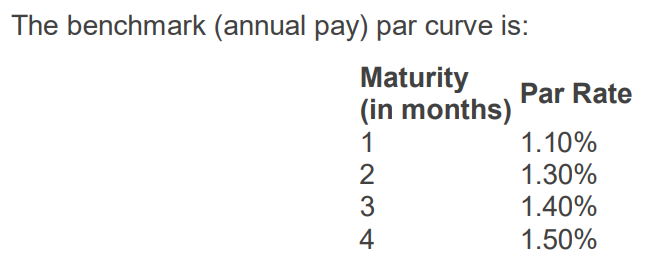

The benchmark (annual pay) par curve is: Maturity Par Rate (in months) 1.10% 1.30% 1.40% 1.50% The benchmark (annual pay) par curve is: Maturity Par Rate (in months) 1.10% 1.30% 1.40% 1.50%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Reforming U.S. Financial Markets Reflections Before And Beyond Dodd Frank

Authors: Randall S. Kroszner, Robert J. Shiller

1st Edition

0262015455, 0262294907, 9780262015455, 9780262294904