Question

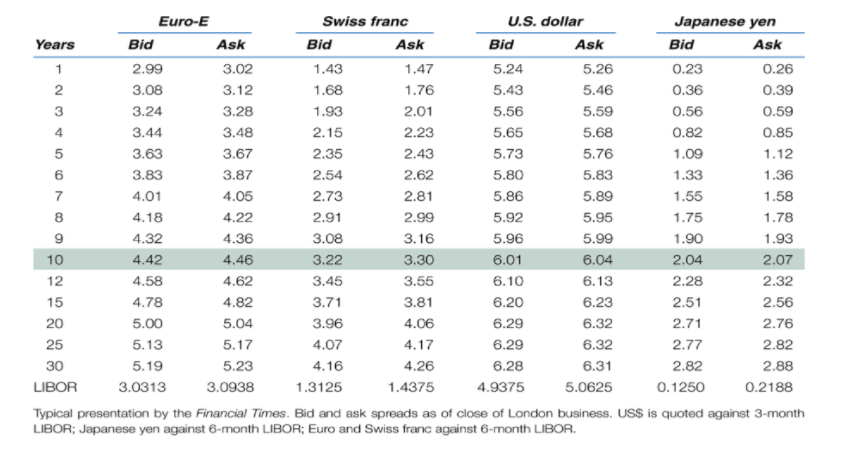

2. Currency swap Using the table of swap rates, assume you enter into a four year swap agreement to receivedollars and pay euro on a

2. Currency swap Using the table of swap rates, assume you enter into a four year swap agreement to receivedollars and pay euro on a notional principal of $1,000,000. The spot exchange rate at the timeof the swap is $1.20/ a. Calculate all principal and interest payments, in both USD and euro, for the life of the

Swap agreement. b. Assume that two years into the swap agreement you decide to unwind the swap agreement and settle it in USD. Assuming that a two-year fixed rate of interest on theUSD is now 4.60 %, and a two-year fixed rate of interest on the euro is now 2.80%, andthe spot rate of exchange is now $1.10/, what is the net present value of the agreement?Who pays whom what?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Building Financial Models

Authors: John Tjia

2nd Edition

0071608893, 978-0071608893