Answered step by step

Verified Expert Solution

Question

1 Approved Answer

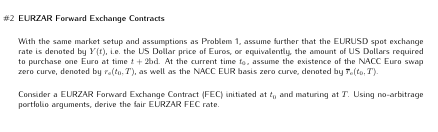

# 2 EURZAR Forward Exchange Contracts With the same market setup and assumptions as Problem 1 , assume further that the EURUSD spot exchange rate

# EURZAR Forward Exchange Contracts

With the same market setup and assumptions as Problem assume further that the EURUSD spot exchange

rate is denoted by ie the US Dollar price of Euros, or equivalently, the amount of US Dollars required

to purchase one Euro at time hd At the current time assume the existence of the NACC Euro swap

zero curve, denoted by as well as the NACC EUR basis zero curve, denoted by

Consider a EURZAR Forward Exchange Contract FEC initiated at and maturing at Using noarbitrage

portialio arguments, derive the fair EURZAR FEC rate.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: R. Charles Moyer, William J. Kretlow, James R. Mcguigan

7th Edition

0538877766, 9780538877763