Answered step by step

Verified Expert Solution

Question

1 Approved Answer

2 Fixed-Income Management (40 Points) Mark the appropriate box to indicate the correct answer. There is only one correct answer. If more than one box

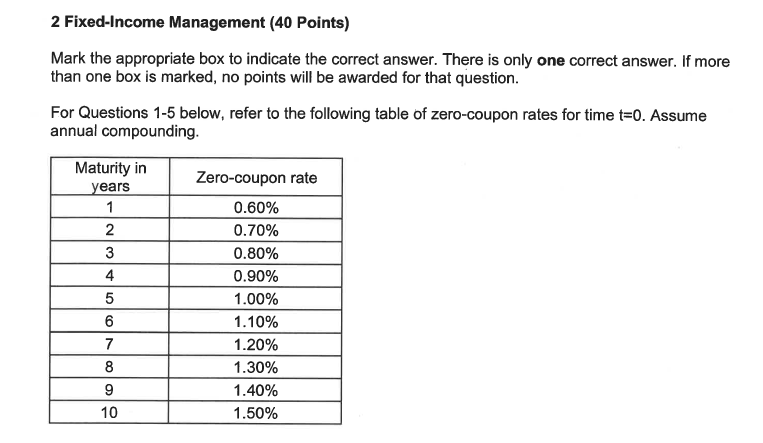

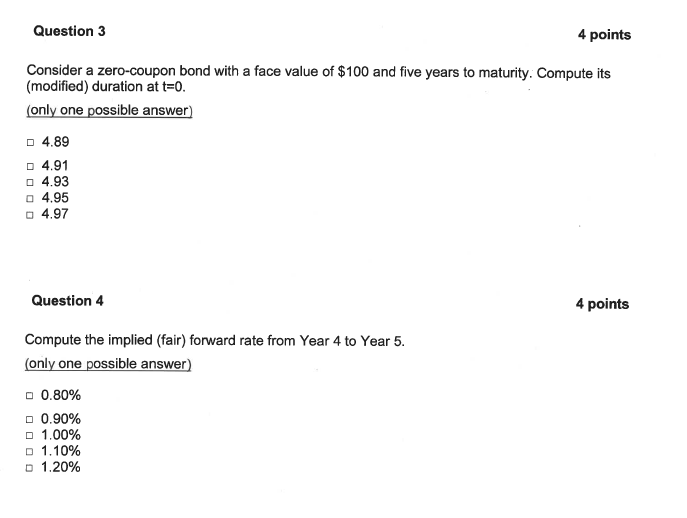

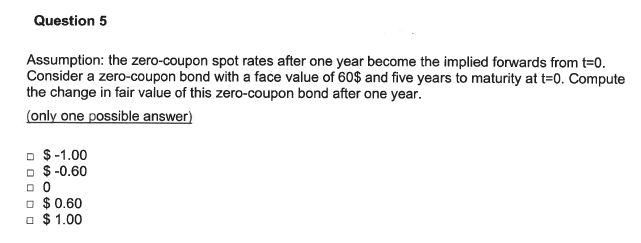

2 Fixed-Income Management (40 Points) Mark the appropriate box to indicate the correct answer. There is only one correct answer. If more than one box is marked, no points will be awarded for that question. For Questions 1-5 below, refer to the following table of zero-coupon rates for time t=0. Assume annual compounding. Consider a zero-coupon bond with a face value of $100 and five years to maturity. Compute its (modified) duration at t=0. (only one possible answer) 4.894.914.934.954.97 Question 4 4 points Compute the implied (fair) forward rate from Year 4 to Year 5. (only one possible answer) 0.80%0.90%1.00%1.10%1.20% Assumption: the zero-coupon spot rates after one year become the implied forwards from t=0. Consider a zero-coupon bond with a face value of 60$ and five years to maturity at t=0. Compute the change in fair value of this zero-coupon bond after one year. (only one possible answer) $1.00$0.600$0.60$1.00 2 Fixed-Income Management (40 Points) Mark the appropriate box to indicate the correct answer. There is only one correct answer. If more than one box is marked, no points will be awarded for that question. For Questions 1-5 below, refer to the following table of zero-coupon rates for time t=0. Assume annual compounding. Consider a zero-coupon bond with a face value of $100 and five years to maturity. Compute its (modified) duration at t=0. (only one possible answer) 4.894.914.934.954.97 Question 4 4 points Compute the implied (fair) forward rate from Year 4 to Year 5. (only one possible answer) 0.80%0.90%1.00%1.10%1.20% Assumption: the zero-coupon spot rates after one year become the implied forwards from t=0. Consider a zero-coupon bond with a face value of 60$ and five years to maturity at t=0. Compute the change in fair value of this zero-coupon bond after one year. (only one possible answer) $1.00$0.600$0.60$1.00

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Learn Forex Trading In 5 Days Forex For Beginners

Authors: Gideon Adewumi ,Igwue Stephen

1st Edition

1980667195, 978-1980667193