Answered step by step

Verified Expert Solution

Question

1 Approved Answer

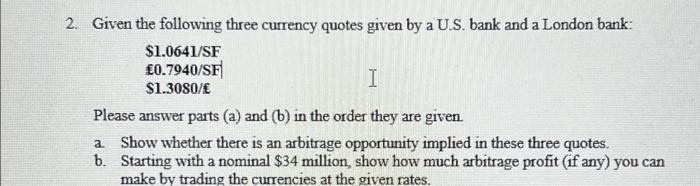

2. Given the following three currency quotes given by a U.S. bank and a London bank: $1.0641/SF 0.7940/SF I $1.3080/ Please answer parts (a) and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Bitcoin Letters Bringing Clarity To The Confusing World Of Blockchain

Authors: Bryan Daugherty ,Gregory Ward

1st Edition

979-8386350444