Question

2. Here you need to show your familiarity with the exponential smoothing forecast calculations, and the calculation of MAE. The first four data points were

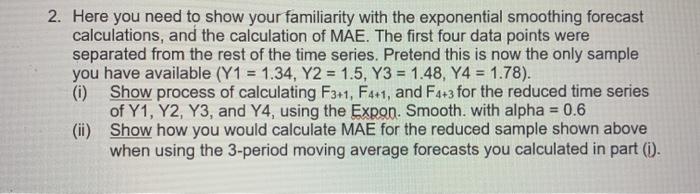

2. Here you need to show your familiarity with the exponential smoothing forecast calculations, and the calculation of MAE. The first four data points were separated from the rest of the time series. Pretend this is now the only sample you have available (Y1 = 1.34, Y2 = 1.5, Y3 = 1.48, Y4 = 1.78).

(i) Show process of calculating F3+1, F4+1, and F4+3 for the reduced time series of Y1, Y2, Y3, and Y4, using the Expon. Smooth. with alpha = 0.6

(ii) Show how you would calculate MAE for the reduced sample shown above when using the 3-period moving average forecasts you calculated in part (i).

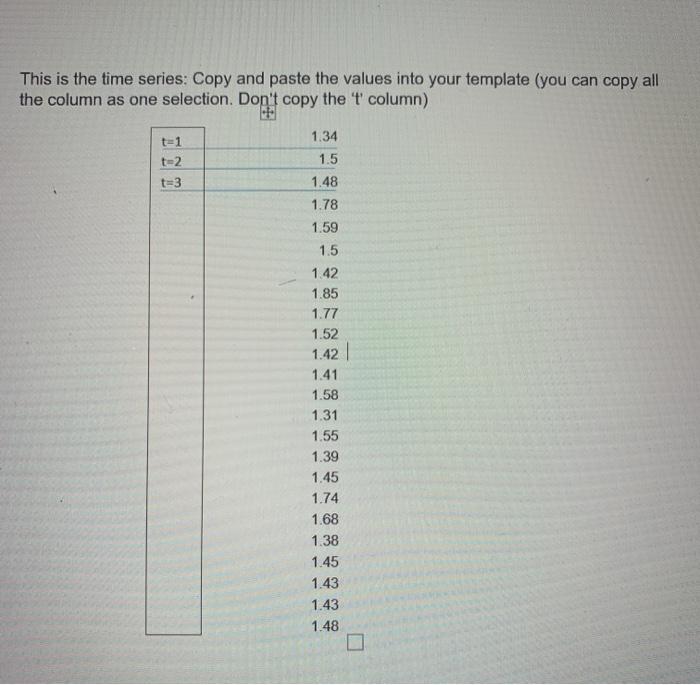

t=1

t=2

t=3

1.34

1.5

1.48

1.78

1.59

1.5

1.42

1.85

1.77

1.52

1.42

1.41

1.58

1.31

1.55

1.39

1.45

1.74

1.68

1.38

1.45

1.43

1.43

1.48

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading For Beginners How To Generate Predictable Income And Make A Living Without Taking Big Risks Even If You Re A Complete Beginner

Authors: Greg Middleton

1st Edition

979-8866955046