Answered step by step

Verified Expert Solution

Question

1 Approved Answer

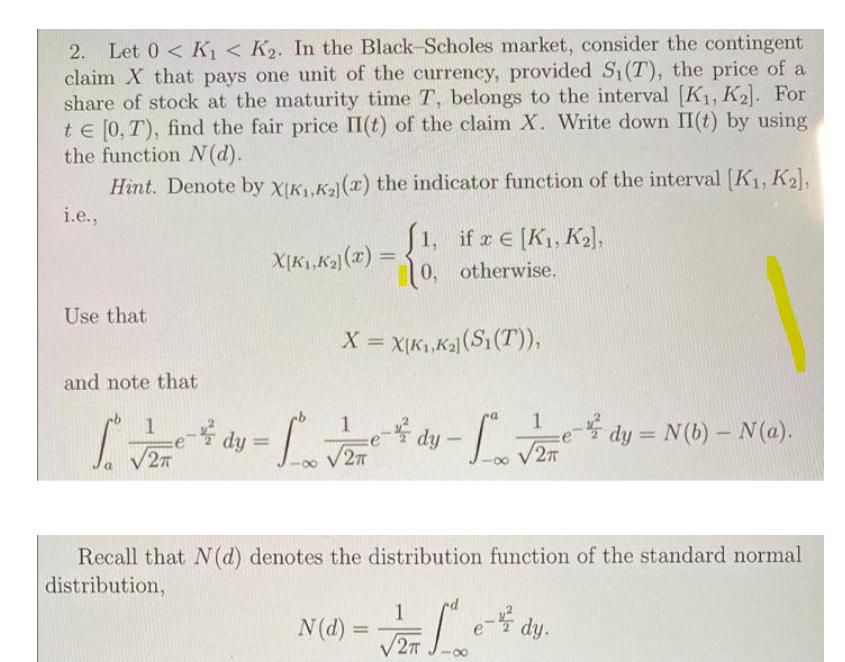

2. Let 0 < K < K2. In the Black-Scholes market, consider the contingent claim X that pays one unit of the currency, provided

2. Let 0 < K < K2. In the Black-Scholes market, consider the contingent claim X that pays one unit of the currency, provided S(T), the price of a share of stock at the maturity time T, belongs to the interval [K1, K2). For te [0, T), find the fair price II(t) of the claim X. Write down II(t) by using the function N(d). Hint. Denote by XIK1.Ka)(x) the indicator function of the interval [K1, K2), i.e., X[K1,K2) (x) : S1, if z E (K1, K2), 0, otherwise. %3D Use that X = X[K1,Ka (S1(T)), and note that dy Le- dy = N(b) N(a). V27 1 dy : %3D %3D 27 27 Recall that N (d) denotes the distribution function of the standard normal distribution, 1 N(d) = dy.

Step by Step Solution

★★★★★

3.38 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

Step by step solution 1A x el ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Linear Algebra

Authors: Peter J. Olver, Cheri Shakiban

1st edition

131473824, 978-0131473829