Answered step by step

Verified Expert Solution

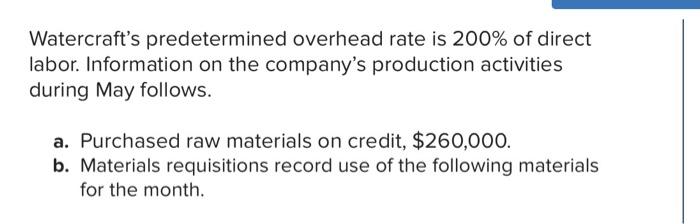

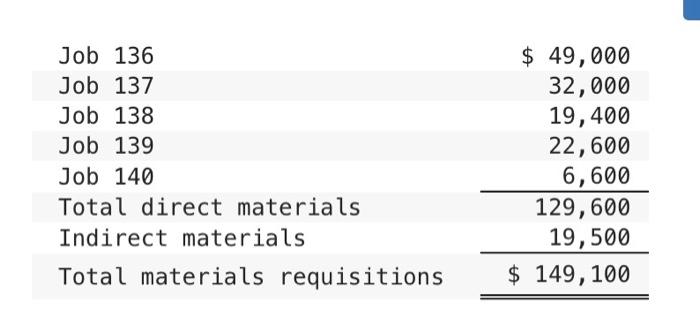

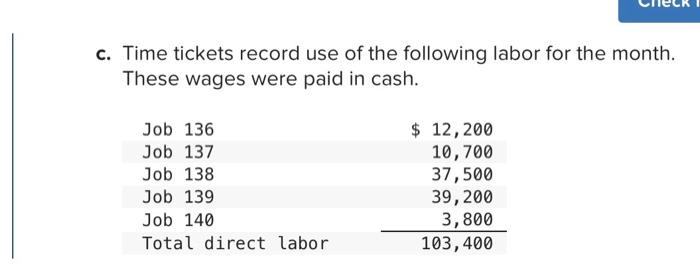

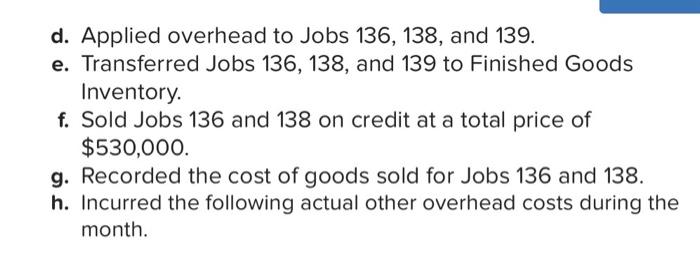

Question

1 Approved Answer

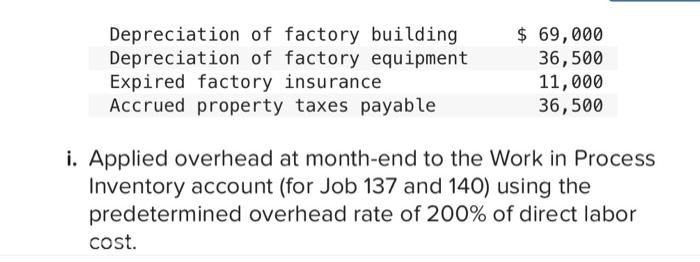

2. Prepare journal entries to record the events and transactions a through i. Journal entry worksheet Record the entry for direct labor, paid in cash.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Criteria For Electronic Document Management Processes And Associated IT Solutions

Authors: Alexander D Balzer, Dr Klaus-Peter Elpel, Volker Feist

5th Edition

3932898281, 978-3932898280