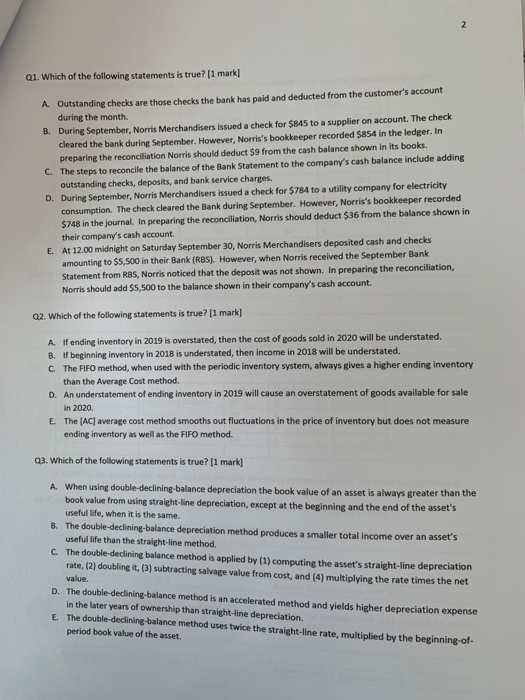

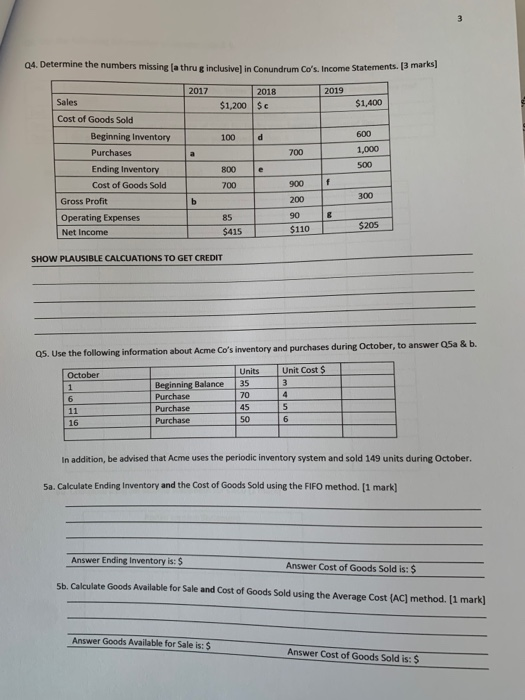

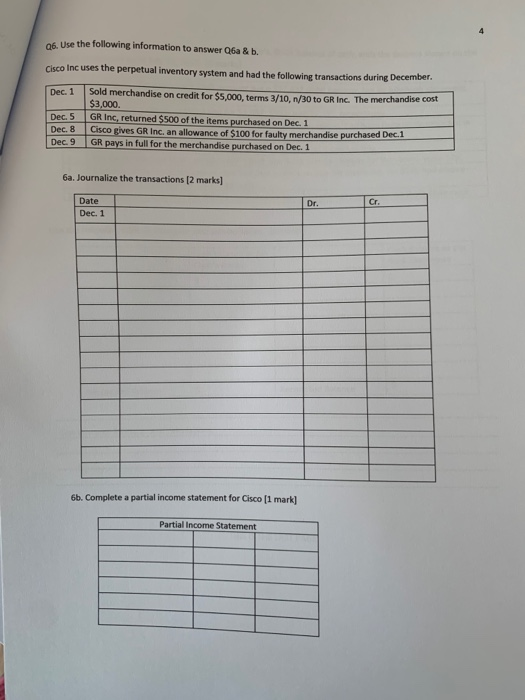

2 Q1. Which of the following statements is true? [1 mark] A. Outstanding checks are those checks the bank has paid and deducted from the customer's account during the month. B. During September, Norris Merchandisers issued a check for $845 to a supplier on account. The check cleared the bank during September. However, Norris's bookkeeper recorded $854 in the ledger. In preparing the reconciliation Norris should deduct $9 from the cash balance shown in its books. C. The steps to reconcile the balance of the Bank Statement to the company's cash balance include adding outstanding checks, deposits, and bank service charges. D. During September, Norris Merchandisers issued a check for $784 to a utility company for electricity consumption. The check cleared the Bank during September. However, Norris's bookkeeper recorded $748 in the journal. In preparing the reconciliation, Norris should deduct $36 from the balance shown in their company's cash account. E. At 12.00 midnight on Saturday September 30, Norris Merchandisers deposited cash and checks amounting to $5,500 in their Bank (RBS). However, when Norris received the September Bank Statement from RBS, Norris noticed that the deposit was not shown. In preparing the reconciliation, Norris should add $5,500 to the balance shown in their company's cash account Q2. Which of the following statements is true? [1 mark] A. If ending inventory in 2019 is overstated, then the cost of goods sold in 2020 will be understated. B. If beginning inventory in 2018 is understated, then income in 2018 will be understated. C. The FIFO method, when used with the periodic inventory system, always gives a higher ending inventory than the Average Cost method. D. An understatement of ending inventory in 2019 will cause an overstatement of goods available for sale in 2020 E. The (AC) average cost method smooths out fluctuations in the price of inventory but does not measure ending inventory as well as the FIFO method. Q3. Which of the following statements is true? [1 mark) A. When using double-declining-balance depreciation the book value of an asset is always greater than the book value from using straight-line depreciation, except at the beginning and the end of the asset's useful life, when it is the same. B. The double-declining-balance depreciation method produces a smaller total income over an asset's useful life than the straight-line method. The double-declining balance method is applied by (1) computing the asset's straight-line depreciation rate, (2) doubling it, (3) subtracting salvage value from cost, and (4) multiplying the rate times the net value. D. The double declining balance method is an accelerated method and yields higher depreciation expense in the later years of ownership than straight-line depreciation. E. The double-declining-balance method uses twice the straight-line rate, multiplied by the beginning-of- period book value of the asset. 3 Q4. Determine the numbers missing (a thrug inclusive) in Conundrum Cos. Income Statements. [3 marks] 2017 2019 2018 $1,200 $ $1,400 100 d 600 a 700 Sales Cost of Goods Sold Beginning Inventory Purchases Ending Inventory Cost of Goods Sold Gross Profit Operating Expenses Net Income 1,000 500 800 e 700 900 1 300 b 200 90 8 85 $415 $110 $205 SHOW PLAUSIBLE CALCUATIONS TO GET CREDIT Q5. Use the following information about Acme Co's inventory and purchases during October, to answer Q5a & b. October 1 Units 35 70 45 50 Beginning Balance Purchase Purchase Purchase Unit Cost $ 3 4 5 6 6 11 16 In addition, be advised that Acme uses the periodic inventory system and sold 149 units during October. Sa. Calculate Ending Inventory and the cost of Goods Sold using the FIFO method. [1 mark] Answer Ending Inventory is: $ Answer Cost of Goods Sold is: $ 5b. Calculate Goods Available for Sale and cost of Goods Sold using the Average Cost (AC) method. [1 mark] Answer Goods Available for Sale is: $ Answer Cost of Goods Sold is: $ 4 26. Use the following information to answer Q6a & b. Cisco Inc uses the perpetual inventory system and had the following transactions during December Dec. 1 Sold merchandise on credit for $5,000, terms 3/10, 1/30 to GR Inc. The merchandise cost $3,000 Dec. 5 GR Inc, returned $500 of the items purchased on Dec. 1 Dec. 8 Cisco gives GR Inc. an allowance of $100 for faulty merchandise purchased Dec. 1 Dec. 9 GR pays in full for the merchandise purchased on Dec. 1 6a. Journalize the transactions [2 marks] Dr. Cr. Date Dec. 1 6b. Complete a partial income statement for Cisco [1 mark] Partial Income Statement 5 27. Use the following information to reconcile Clark Co's. Book Balance of cash, with the Balance shown on the Bank Statement as of July 31, 2015. (6 marks] a On July 31, the company's Cash account has a $27,497 debit balance, but its July bank statement shows a $27,158 cash Balance. b There were 3 checks outstanding for $1,482; $382; and $2,281, respectively. Clark found that a check correctly written for $1,270 of supplies, had been incorrectly recorded in Clark's accounting records as $1,720. d The Bank collected an $8,000 Note for Clark. Clark had not recorded this. The Bank returned Clark, an $805 NSF Check and Bank Service charges for the month were $70. A review of the bank statement revealed that a check written by Clarke Inc, for $545 had errone- ously been drawn against Clark's account. Clark placed $11,514 in the Bank's night deposit box. This did not appear on the Bank Statement e Use the following table to Illustrate your reconciliation. [6 marks] Cash Balance as per Clark's Books Cash Balance as per Bank Statement $ $ Reconciled Balance $ Reconciled Balance $ Use this area for notes and calculations. THIS IS THE LAST PAGE