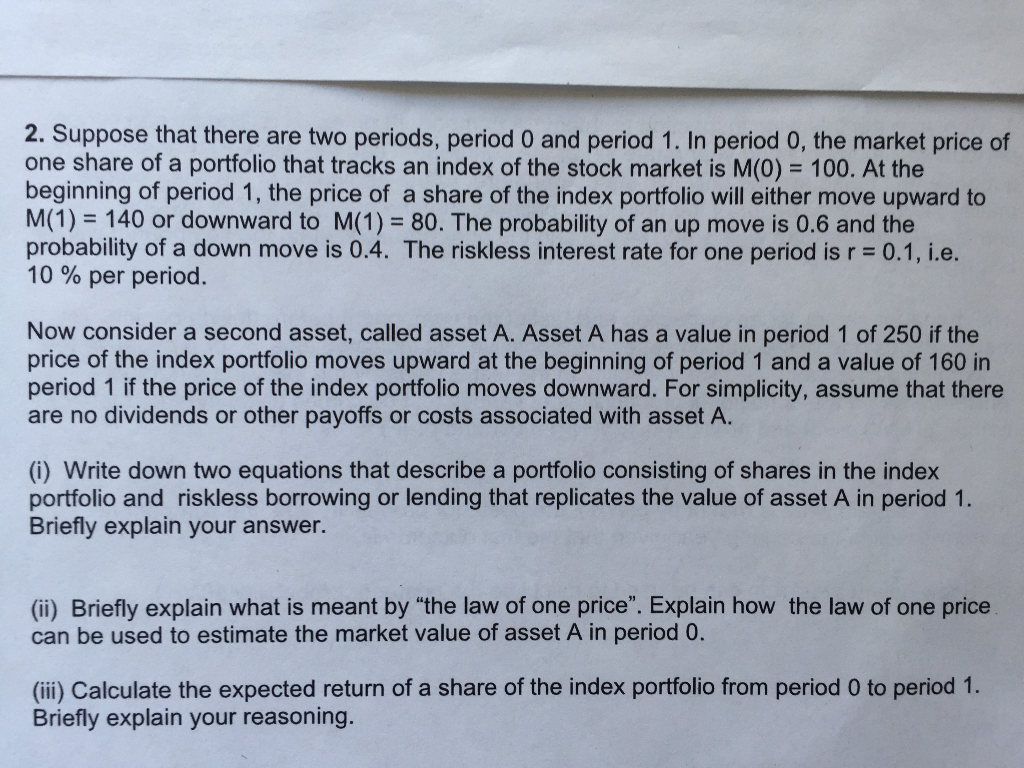

2. Suppose that there are two periods, period 0 and period 1. In period 0, the market price of one share of a portfolio that tracks an index of the stock market is M(0) 100. At the beginning of period 1, the price of a share of the index portfolio will either move upward to M(1) 140 or downward to M(1) 80. The probability of an up move is 0.6 and the probability of a down move is 0.4. The riskless interest rate for one period is r 0.1, i.e. 10 % per period. Now consider a second asset, called asset A. Asset A has a value in period 1 of 250 if the price of the index portfolio moves upward at the beginning of period 1 and a value of 160 in period 1 if the price of the index portfolio moves downward. For simplicity, assume that there are no dividends or other payoffs or costs associated with asset A. (i) Write down two equations that describe a portfolio consisting of shares in the index portfolio and riskless borrowing or lending that replicates the value of asset A in period 1. Briefly explain your answer. (ii) Briefly explain what is meant by "the law of one price". Explain how the law of one price can be used to estimate the market value of asset A in period 0. (ii) Calculate the expected return of a share of the index portfolio from period 0 to period 1. Briefly explain your reasoning. 2. Suppose that there are two periods, period 0 and period 1. In period 0, the market price of one share of a portfolio that tracks an index of the stock market is M(0) 100. At the beginning of period 1, the price of a share of the index portfolio will either move upward to M(1) 140 or downward to M(1) 80. The probability of an up move is 0.6 and the probability of a down move is 0.4. The riskless interest rate for one period is r 0.1, i.e. 10 % per period. Now consider a second asset, called asset A. Asset A has a value in period 1 of 250 if the price of the index portfolio moves upward at the beginning of period 1 and a value of 160 in period 1 if the price of the index portfolio moves downward. For simplicity, assume that there are no dividends or other payoffs or costs associated with asset A. (i) Write down two equations that describe a portfolio consisting of shares in the index portfolio and riskless borrowing or lending that replicates the value of asset A in period 1. Briefly explain your answer. (ii) Briefly explain what is meant by "the law of one price". Explain how the law of one price can be used to estimate the market value of asset A in period 0. (ii) Calculate the expected return of a share of the index portfolio from period 0 to period 1. Briefly explain your reasoning