Answered step by step

Verified Expert Solution

Question

1 Approved Answer

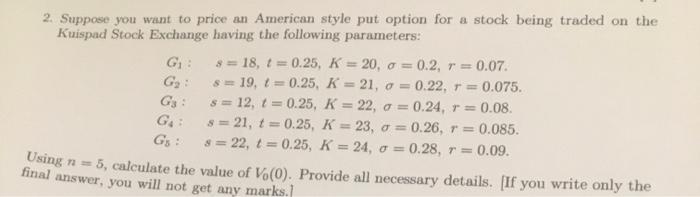

2. Suppose you want to price an American style put option for a stock being traded on the Kuispad Stock Exchange having the following parameters:

2. Suppose you want to price an American style put option for a stock being traded on the Kuispad Stock Exchange having the following parameters: G: G: G3: G: G5: S= = 18, t = 0.25, K = 20, o = 0.2, r = 0.07. s = 19, t = 0.25, K = 21, o = 0.22, r = 0.075. s = 12, t = 0.25, K = 22, o = 0.24, r = 0.08. s = 21, t = 0.25, K = 23, o = 0.26, r = 0.085. 0.28, r = 0.09. s = 22, t = 0.25, K = 24, o = Using n = 5, calculate the value of Vo(0). Provide all necessary details. [If you write only the final answer, you will not get any marks.]

please use information based on G4 only

2. Suppose you want to price an American style put option for a stock being traded on the Kuispad Stock Exchange having the following parameters: G1:G2:G3:G4:Gs:s=18,t=0.25,K=20,=0.2,r=0.07.s=19,t=0.25,K=21,=0.22,r=0.075.s=12,t=0.25,K=22,=0.24,r=0.08.s=21,t=0.25,K=23,=0.26,r=0.085.s=22,t=0.25,K=24,=0.28,r=0.09. Using n=5, calculate the value of V0(0). Provide all necessary details. [If you write only the final answer, you will not get any marks.l Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Valuation

Authors: James R. Hitchner

4th Edition

1119286603, 978-1119286608