Answered step by step

Verified Expert Solution

Question

1 Approved Answer

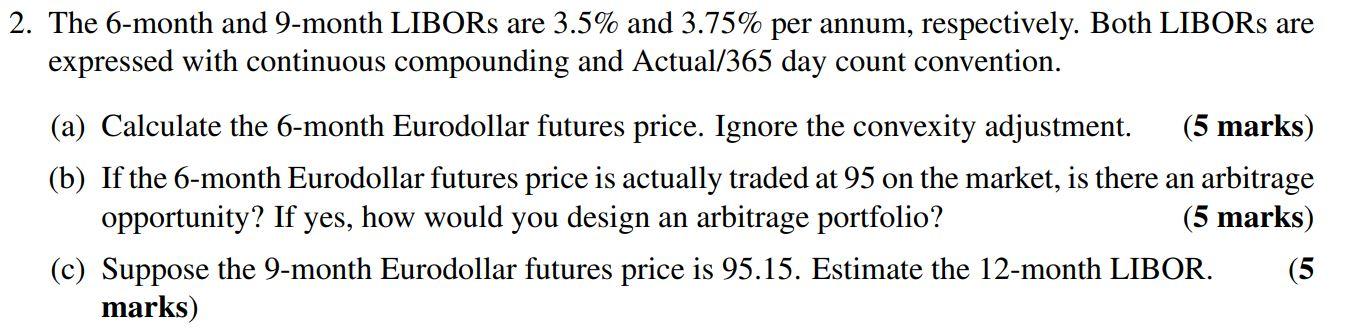

2. The 6-month and 9-month LIBORs are 3.5% and 3.75% per annum, respectively. Both LIBORs are expressed with continuous compounding and Actual/365 day count convention.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Financial Management An Applied Approach

Authors: Jeffrey R Cornwall, David O Vang, Jean M Hartman

5th Edition

0367335417, 978-0367335410