Question

2. There are only two investors and two risky assets (Stock A and B) in the market. The investors are Mr. Black and Mrs. White.

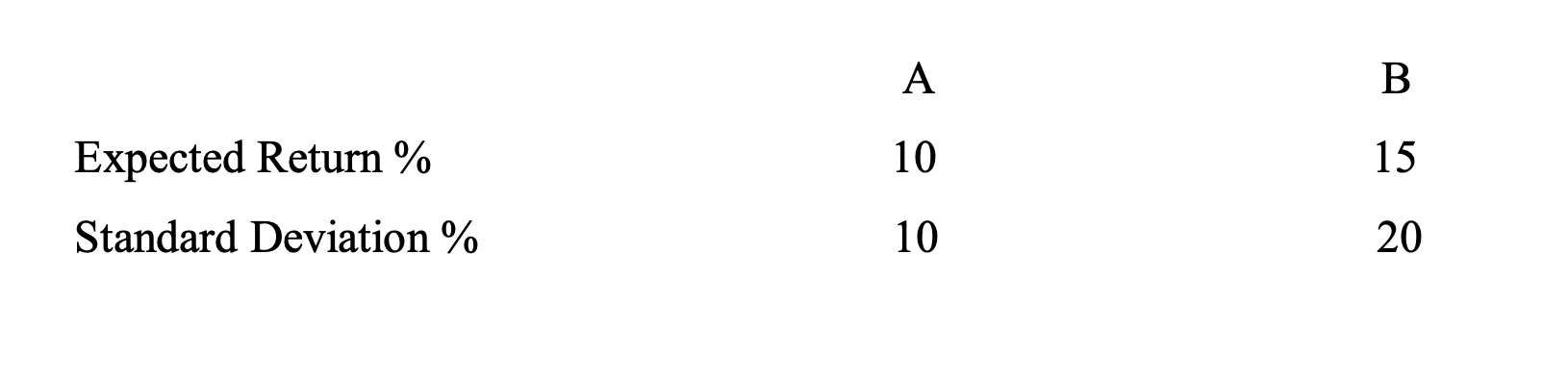

2. There are only two investors and two risky assets (Stock A and B) in the market. The investors are Mr. Black and Mrs. White. Mr. Black invests 6 billion dollars on Stock A, $4 billion on Stock B and $1 billion on risk-free bank deposit while Mrs. White spends $7.5 billion buying stock A, $5 billion buying B and $10 billion on risk-free bank deposit. The returns of A and B are as follows:

The correlation between two returns is 0.

i) What is the market portfolio (of risky assets)?

ii) Suppose the CAPM holds, what is the risk-free return in equilibrium?

iii)What are the numerical equations for the CML and SML of the market?

iv) Draw the diagrams of CML and SML. Do Asset A and B lie on them?

Expected Return % Standard Deviation %Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Term Structure Models A Graduate Course

Authors: Damir Filipovic

2009th Edition

364226915X, 978-3642269158