Answered step by step

Verified Expert Solution

Question

1 Approved Answer

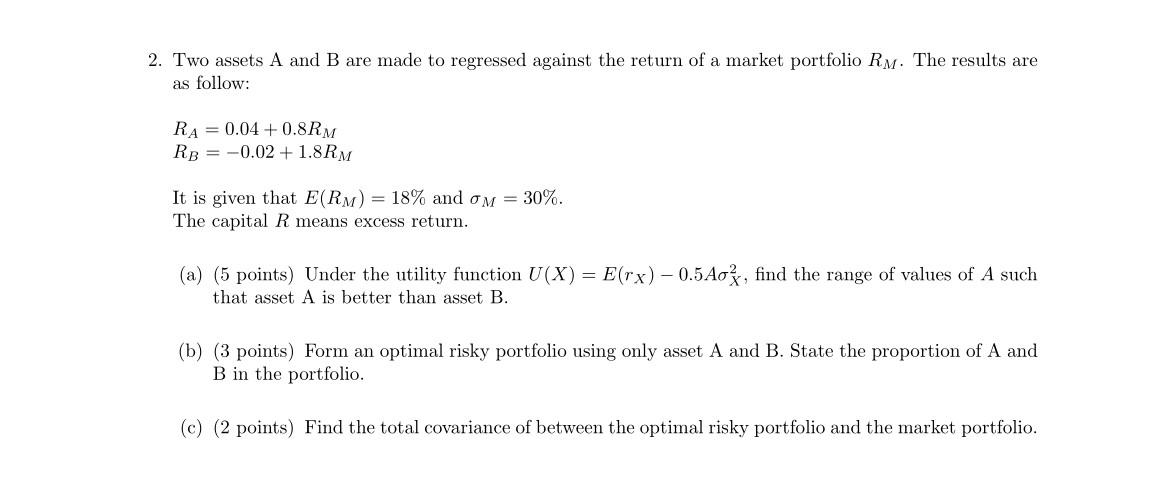

2. Two assets A and B are made to regressed against the return of a market portfolio Rm. The results are as follow: RA =

2. Two assets A and B are made to regressed against the return of a market portfolio Rm. The results are as follow: RA = 0.04+0.8RM RB = -0.02 +1.8RM It is given that E(RM) = 18% and om = 30%. The capital R means excess return. (a) (5 points) Under the utility function U(X) = E(rx) - 0.5Ao, find the range of values of A such that asset A is better than asset B. (b) (3 points) Form an optimal risky portfolio using only asset A and B. State the proportion of A and B in the portfolio. (c) (2 points) Find the total covariance of between the optimal risky portfolio and the market portfolio. 2. Two assets A and B are made to regressed against the return of a market portfolio Rm. The results are as follow: RA = 0.04+0.8RM RB = -0.02 +1.8RM It is given that E(RM) = 18% and om = 30%. The capital R means excess return. (a) (5 points) Under the utility function U(X) = E(rx) - 0.5Ao, find the range of values of A such that asset A is better than asset B. (b) (3 points) Form an optimal risky portfolio using only asset A and B. State the proportion of A and B in the portfolio. (c) (2 points) Find the total covariance of between the optimal risky portfolio and the market portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Big Tech In Finance

Authors: Igor Pejic

1st Edition

139860898X, 978-1398608986