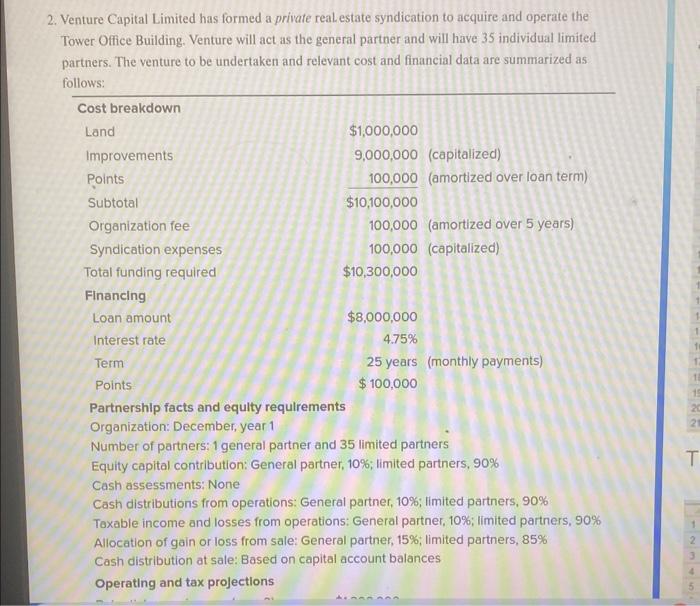

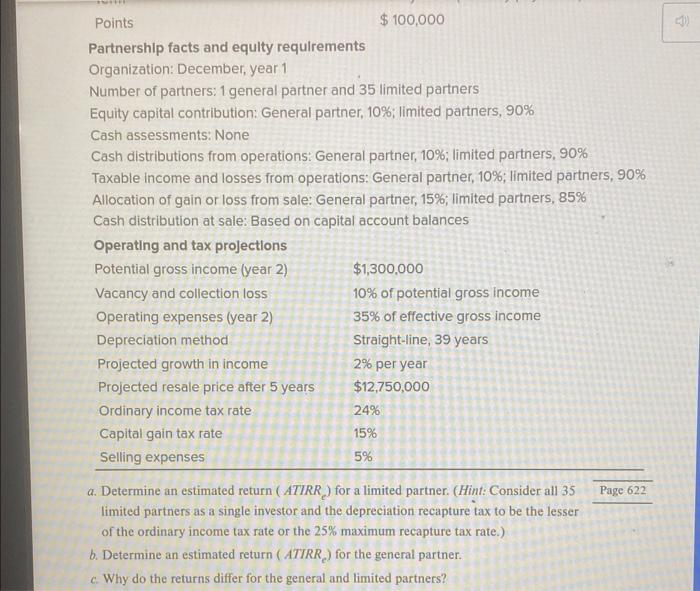

2. Venture Capital Limited has formed a private real estate syndication to acquire and operate the Tower Office Building. Venture will act as the general partner and will have 35 individual limited partners. The venture to be undertaken and relevant cost and financial data are summarized as fillowe: Partnershlp facts and equlty requlrements Organization: December, year 1 Number of partners: 1 general partner and 35 limited parthers Equity capital contribution: General partner, 10\%; limited partners, 90% Cash assessments: None Cash distributions from operations: General partner, 10\%: limited parthers, 90% Toxable income and losses from operations: General partner, 10\%; limited partners, 90% Allocation of gain or loss from sale: General partner, 15%; limited partners, 85% Cash distribution at sale: Based on capital account balances Operating and tax projections Points Partnership facts and equity requirements Organization: December, year 1 Number of partners: 1 general partner and 35 limited partners Equity capital contribution: General partner, 10\%; limited partners, 90% Cash assessments: None Cash distributions from operations: General partner, 10%; limited parthers, 90% Taxable income and losses from operations: General partner, 10\%; limited partners, 90% Allocation of gain or loss from sale: General partner, 15\%; limited partners, 85% Cash distribution at sale: Based on capital account balances a. Determine an estimated return ( ATIRRe ) for a limited partner. (Hint: Consider all 35 Page 622 limited partners as a single investor and the depreciation recapture tax to be the lesser of the ordinary income tax rate or the 25% maximum recapture tax rate.) b. Determine an estimated return (ATIRRe) for the general partner. c. Why do the returns differ for the general and limited partners? 2. Venture Capital Limited has formed a private real estate syndication to acquire and operate the Tower Office Building. Venture will act as the general partner and will have 35 individual limited partners. The venture to be undertaken and relevant cost and financial data are summarized as fillowe: Partnershlp facts and equlty requlrements Organization: December, year 1 Number of partners: 1 general partner and 35 limited parthers Equity capital contribution: General partner, 10\%; limited partners, 90% Cash assessments: None Cash distributions from operations: General partner, 10\%: limited parthers, 90% Toxable income and losses from operations: General partner, 10\%; limited partners, 90% Allocation of gain or loss from sale: General partner, 15%; limited partners, 85% Cash distribution at sale: Based on capital account balances Operating and tax projections Points Partnership facts and equity requirements Organization: December, year 1 Number of partners: 1 general partner and 35 limited partners Equity capital contribution: General partner, 10\%; limited partners, 90% Cash assessments: None Cash distributions from operations: General partner, 10%; limited parthers, 90% Taxable income and losses from operations: General partner, 10\%; limited partners, 90% Allocation of gain or loss from sale: General partner, 15\%; limited partners, 85% Cash distribution at sale: Based on capital account balances a. Determine an estimated return ( ATIRRe ) for a limited partner. (Hint: Consider all 35 Page 622 limited partners as a single investor and the depreciation recapture tax to be the lesser of the ordinary income tax rate or the 25% maximum recapture tax rate.) b. Determine an estimated return (ATIRRe) for the general partner. c. Why do the returns differ for the general and limited partners