Answered step by step

Verified Expert Solution

Question

1 Approved Answer

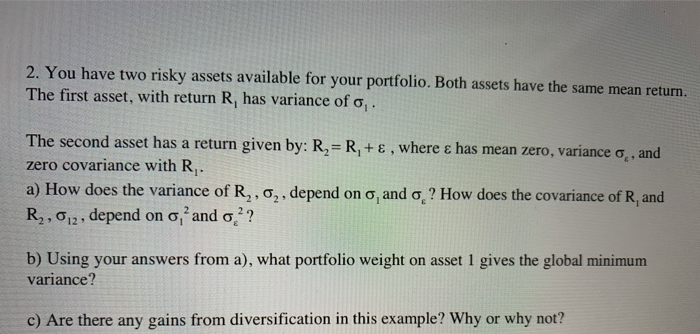

2. You have two risky assets available for your portfolio. Both assets have the same mean return. The first asset, with return R, has variance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secretarial Audit Compliance Management And Due Diligence CS Professional New Course

Authors: AJ

16th Edition

9390303842, 978-9390303847