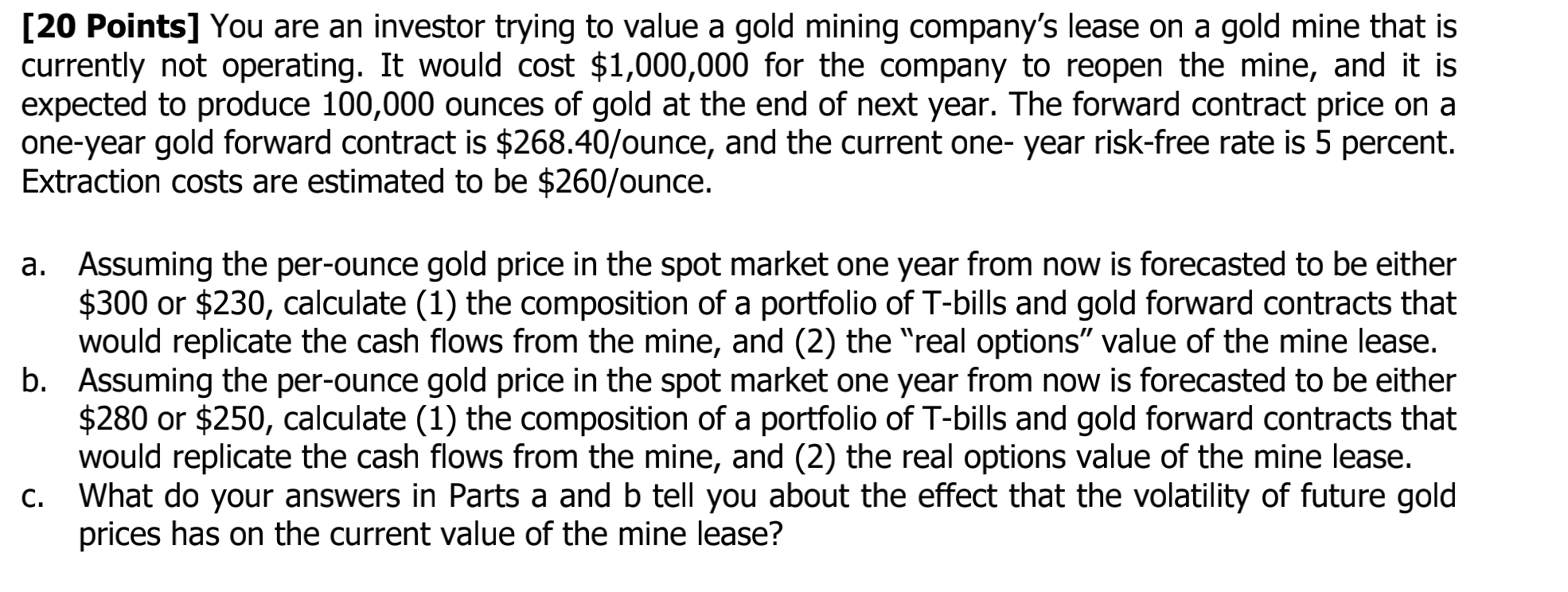

[20 Points] You are an investor trying to value a gold mining company's lease on a gold mine that is currently not operating. It would cost $1,000,000 for the company to reopen the mine, and it is expected to produce 100,000 ounces of gold at the end of next year. The forward contract price on a one-year gold forward contract is $268.40/ounce, and the current one-year risk-free rate is 5 percent. Extraction costs are estimated to be $260/ounce. a. Assuming the per-ounce gold price in the spot market one year from now is forecasted to be either $300 or $230, calculate (1) the composition of a portfolio of T-bills and gold forward contracts that would replicate the cash flows from the mine, and (2) the "real options" value of the mine lease. b. Assuming the per-ounce gold price in the spot market one year from now is forecasted to be either $280 or $250, calculate (1) the composition of a portfolio of T-bills and gold forward contracts that would replicate the cash flows from the mine, and (2) the real options value of the mine lease. C. What do your answers in Parts a and b tell you about the effect that the volatility of future gold prices has on the current value of the mine lease? [20 Points] You are an investor trying to value a gold mining company's lease on a gold mine that is currently not operating. It would cost $1,000,000 for the company to reopen the mine, and it is expected to produce 100,000 ounces of gold at the end of next year. The forward contract price on a one-year gold forward contract is $268.40/ounce, and the current one-year risk-free rate is 5 percent. Extraction costs are estimated to be $260/ounce. a. Assuming the per-ounce gold price in the spot market one year from now is forecasted to be either $300 or $230, calculate (1) the composition of a portfolio of T-bills and gold forward contracts that would replicate the cash flows from the mine, and (2) the "real options" value of the mine lease. b. Assuming the per-ounce gold price in the spot market one year from now is forecasted to be either $280 or $250, calculate (1) the composition of a portfolio of T-bills and gold forward contracts that would replicate the cash flows from the mine, and (2) the real options value of the mine lease. C. What do your answers in Parts a and b tell you about the effect that the volatility of future gold prices has on the current value of the mine lease