Answered step by step

Verified Expert Solution

Question

1 Approved Answer

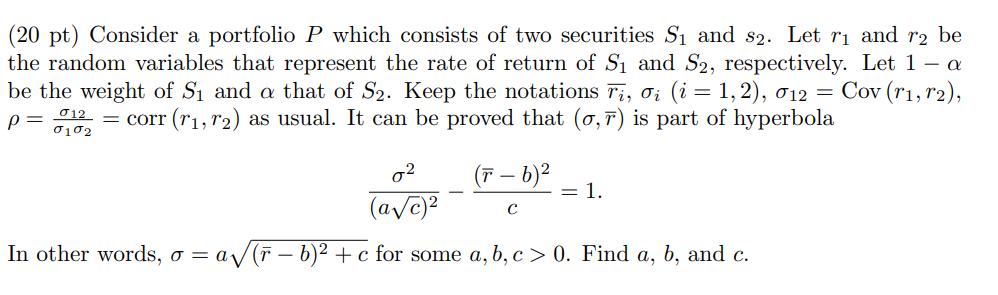

(20 pt) Consider a portfolio P which consists of two securities S and s2. Let r and r2 be the random variables that represent

(20 pt) Consider a portfolio P which consists of two securities S and s2. Let r and r2 be the random variables that represent the rate of return of S and S2, respectively. Let 1 - a be the weight of S and a that of S. Keep the notations Ti, oi (i = 1,2), 012 = Cov (r1, 72), 12 = corr (r, r2) as usual. It can be proved that (0,7) is part of hyperbola p= 0102 (T - b) C 02 (ac) In other words, o = a(r-b) + c for some a, b, c > 0. Find a, b, and c. = 1.

Step by Step Solution

★★★★★

3.42 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

The portfolio return is given byrP 1 ar1 ar2 The expected return of the portfolio isEr...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Engineering Mathematics

Authors: ERWIN KREYSZIG

9th Edition

0471488852, 978-0471488859