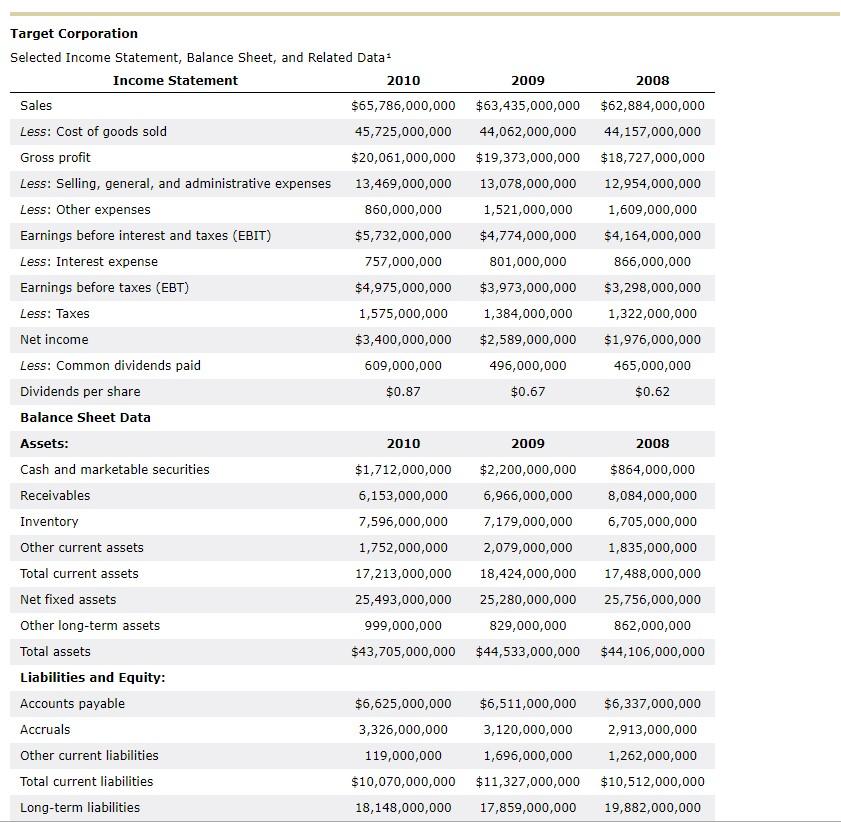

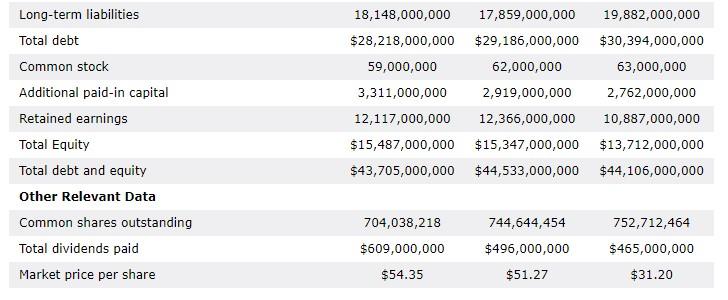

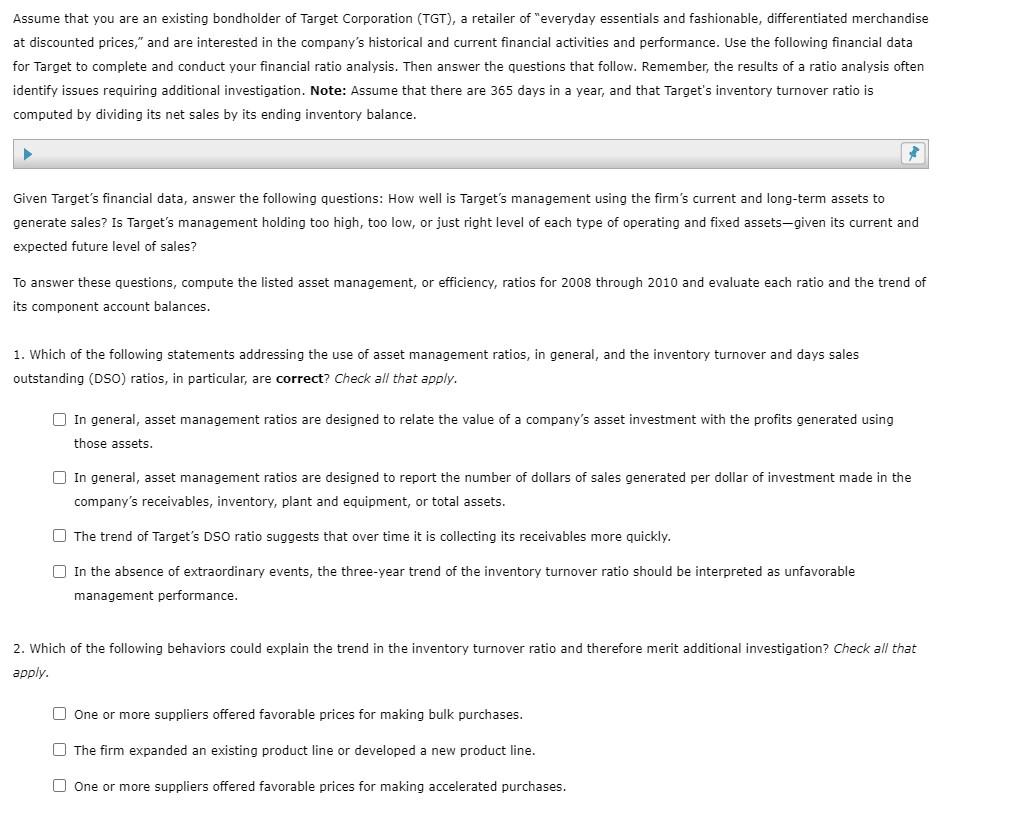

2008 $62,884,000,000 44,157,000,000 $18,727,000,000 12,954,000,000 1,609,000,000 $4,164,000,000 866,000,000 $3,298,000,000 1,322,000,000 $1,976,000,000 465,000,000 $0.62 Target Corporation Selected Income Statement, Balance Sheet, and Related Data- Income Statement 2010 2009 Sales $65,786,000,000 $63,435,000,000 Less: Cost of goods sold 45,725,000,000 44,062,000,000 Gross profit $20,061,000,000 $19,373,000,000 Less: Selling, general, and administrative expenses 13,469,000,000 13,078,000,000 Less: Other expenses 860,000,000 1,521,000,000 Earnings before interest and taxes (EBIT) $5,732,000,000 $4,774,000,000 Less: Interest expense 757,000,000 801,000,000 Earnings before taxes (EBT) $4,975,000,000 $3,973,000,000 Less: Taxes 1,575,000,000 1,384,000,000 Net income $3,400,000,000 $2,589,000,000 Less: Common dividends paid 609,000,000 496,000,000 Dividends per share $0.87 $0.67 Balance Sheet Data Assets: 2010 2009 Cash and marketable securities $1,712,000,000 $2,200,000,000 Receivables 6,153,000,000 6,966,000,000 Inventory 7,596,000,000 7,179,000,000 Other current assets 1,752,000,000 2,079,000,000 Total current assets 17,213,000,000 18,424,000,000 Net fixed assets 25,493,000,000 25,280,000,000 Other long-term assets 999,000,000 829,000,000 Total assets $43,705,000,000 $44,533,000,000 Liabilities and Equity: Accounts payable $6,625,000,000 $6,511,000,000 Accruals 3,326,000,000 3,120,000,000 Other current liabilities 119,000,000 1,696,000,000 Total current liabilities $10,070,000,000 $11,327,000,000 Long-term liabilities 18,148,000,000 17,859,000,000 2008 $864,000,000 8,084,000,000 6,705,000,000 1,835,000,000 17,488,000,000 25,756,000,000 862,000,000 $44,106,000,000 $6,337,000,000 2,913,000,000 1,262,000,000 $10,512,000,000 19,882,000,000 Long-term liabilities Total debt Common stock Additional paid-in capital Retained earnings Total Equity Total debt and equity Other Relevant Data Common shares outstanding Total dividends paid Market price per share 18,148,000,000 17,859,000,000 $28,218,000,000 $29,186,000,000 59,000,000 62,000,000 3,311,000,000 2,919,000,000 12,117,000,000 12,366,000,000 $15,487,000,000 $15,347,000,000 $43,705,000,000 $44,533,000,000 19,882,000,000 $30,394,000,000 63,000,000 2,762,000,000 10,887,000,000 $13,712,000,000 $44,106,000,000 744,644,454 752,712,464 704,038,218 $609,000,000 $496,000,000 $465,000,000 $31.20 $54.35 $51.27 Assume that you are an existing bondholder of Target Corporation (TGT), a retailer of "everyday essentials and fashionable, differentiated merchandise at discounted prices," and are interested in the company's historical and current financial activities and performance. Use the following financial data for Target to complete and conduct your financial ratio analysis. Then answer the questions that follow. Remember, the results of a ratio analysis often identify issues requiring additional investigation. Note: Assume that there are 365 days in a year, and that Target's inventory turnover ratio is computed by dividing its net sales by its ending inventory balance. Given Target's financial data, answer the following questions: How well is Target's management using the firm's current and long-term assets to generate sales? Is Target's management holding too high, too low, or just right level of each type of operating and fixed assets-given its current and expected future level of sales? To answer these questions, compute the listed asset management, or efficiency, ratios for 2008 through 2010 and evaluate each ratio and the trend of its component account balances. 1. Which of the following statements addressing the use of asset management ratios, in general, and the inventory turnover and days sales outstanding (DSO) ratios, in particular, are correct? Check all that apply. In general, asset management ratios are designed to relate the value of a company's asset investment with the profits generated using those assets. In general, asset management ratios are designed to report the number of dollars of sales generated per dollar of investment made in the company's receivables, inventory, plant and equipment, or total assets. The trend of Target's DSO ratio suggests that over time it is collecting its receivables more quickly. In the absence of extraordinary events, the three-year trend of the inventory turnover ratio should be interpreted as unfavorable management performance. 2. Which of the following behaviors could explain the trend in the inventory turnover ratio and therefore merit additional investigation? Check all that apply. One or more suppliers offered favorable prices for making bulk purchases. The firm expanded an existing product line or developed a new product line. One or more suppliers offered favorable prices for making accelerated purchases. 3. Consider the trend of Target's DSO ratios, as well as the pattern of its Sales and Accounts receivable balances. (Note: Round all intermediate and final calculations to two decimal places.) Target Corporation Asset Management Ratios Inventory turnover ratio 2010 2009 2008 DSO 2010 2009 2008 Fixed asset turnover ratio 2010 days days days 2009 III 2008 Total asset turnover ratio 2010 2009 2008 If Target is making fewer credit sales because management is concerned about future economic conditions and preventing defaults and unrecoverable accounts receivable, then this finding could reflect favorably in your assessment of management's performance. On the other hand, if credit sales are declining because sales associates in the company's stores are failing to encourage customers to open new Target credit cards, then this isn't a favorable behavior because the company may be opportunities for greater future sales and earned interest income. 4. Which statement addressing Target's fixed asset turnover ratios or its component accounts is correct? Target's fixed asset turnover ratio should be computed using the total historical cost of its fixed assets, which means that the ratio should not reflect the accumulated depreciation, or age, of its fixed assets. The reason why the fixed asset turnover ratio increases from 2009 to 2010 is that the Sales account increases by 3.71%, while the Net fixed asset account increases by only 0.84%. In general, a higher, rather than a lower, fixed asset turnover ratio will reflect on management's performance. However, the practice of generating ever-greater sales dollars using the same stock of property, plant, and equipment can be taken to extreme. Which practice would increase a company's fixed asset turnover ratio to the detriment of the company's long-term viability and profitability? O A company doesn't replace worn-out plant and equipment and operates the remaining assets over additional work shifts. A company cuts back on the downtime and maintenance and repair activities necessary to preserve the performance of the property and equipment. 5. The trend of the total asset turnover ratio indicates that Target is moderately successful in generating sales dollars using its entire holding of assets. In general, it earns $1.42 to $1.51 of for every dollar of assets owned. 6. Given these insights and information, which of the following statements are correct? Check all that apply. Possible explanations for inventories that accumulate faster than the firm's sales include holding obsolete, missing, or unsalable items, as well as bulk purchases made to capitalize on discounts from suppliers, and preparation for busy seasonal sales periods (such as back-to- school and the Christmas holiday). Target's increase in inventory holdings helps explain the trend in the company's liquidity ratios. Without knowing the trend of the company's gross fixed assets, several possible explanations for the trend of the fixed asset turnover ratio could include the writing-off of old, no salvageable equipment or a switch from straight-line depreciation to some form of accelerated depreciation (which would increase the company's annual depreciation expense and affect its accumulated depreciation account). In general and all other considerations being equal, Target should prefer a smaller, rather than a larger, value for its turnover ratios. Between 2008 and 2010, Target reduced the delay associated with collecting its accounts receivable by approximately 12 days. This is a positive finding because it can lead to fewer uncollectible accounts