Answered step by step

Verified Expert Solution

Question

1 Approved Answer

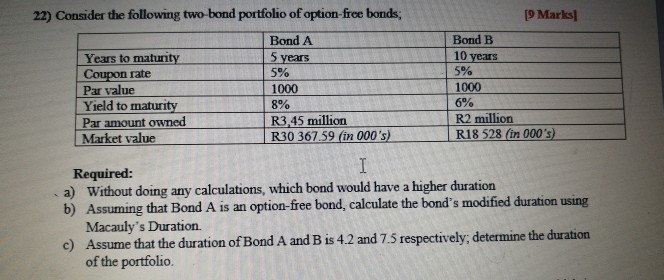

22) Consider the following two bond portfolio of option free bonds, [9 Marks Years to maturity Coupon rate Par value Yield to maturity Par amount

22) Consider the following two bond portfolio of option free bonds, [9 Marks Years to maturity Coupon rate Par value Yield to maturity Par amount owned Market value Bond A 5 years 5% 1000 8% R3,45 million R30 367.59 (in 000's) Bond B 10 years 5% 1000 6% R2 million R18 528 (in 000's) Required: I a) Without doing any calculations, which bond would have a higher duration b) Assuming that Bond A is an option-free bond, calculate the bond's modified duration using Macauly's Duration c) Assume that the duration of Bond A and B is 4.2 and 7.5 respectively, determine the duration of the portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secured Finance Transactions

Authors: Dominic RM Griffiths

2nd Edition

1787425142, 978-1787425149