Answered step by step

Verified Expert Solution

Question

1 Approved Answer

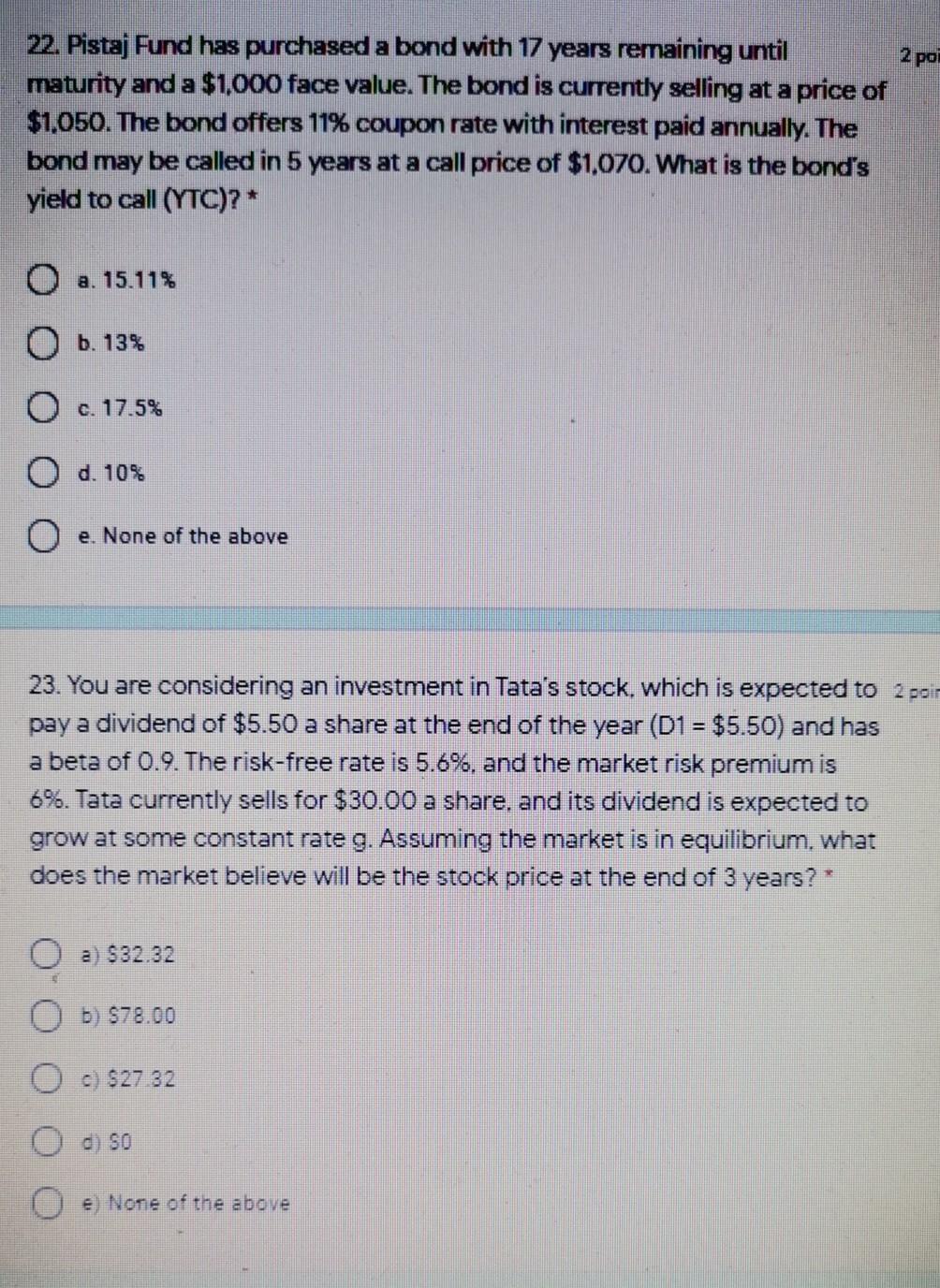

22. Pistaj Fund has purchased a bond with 17 years remaining until 2 po maturity and a $1,000 face value. The bond is currently selling

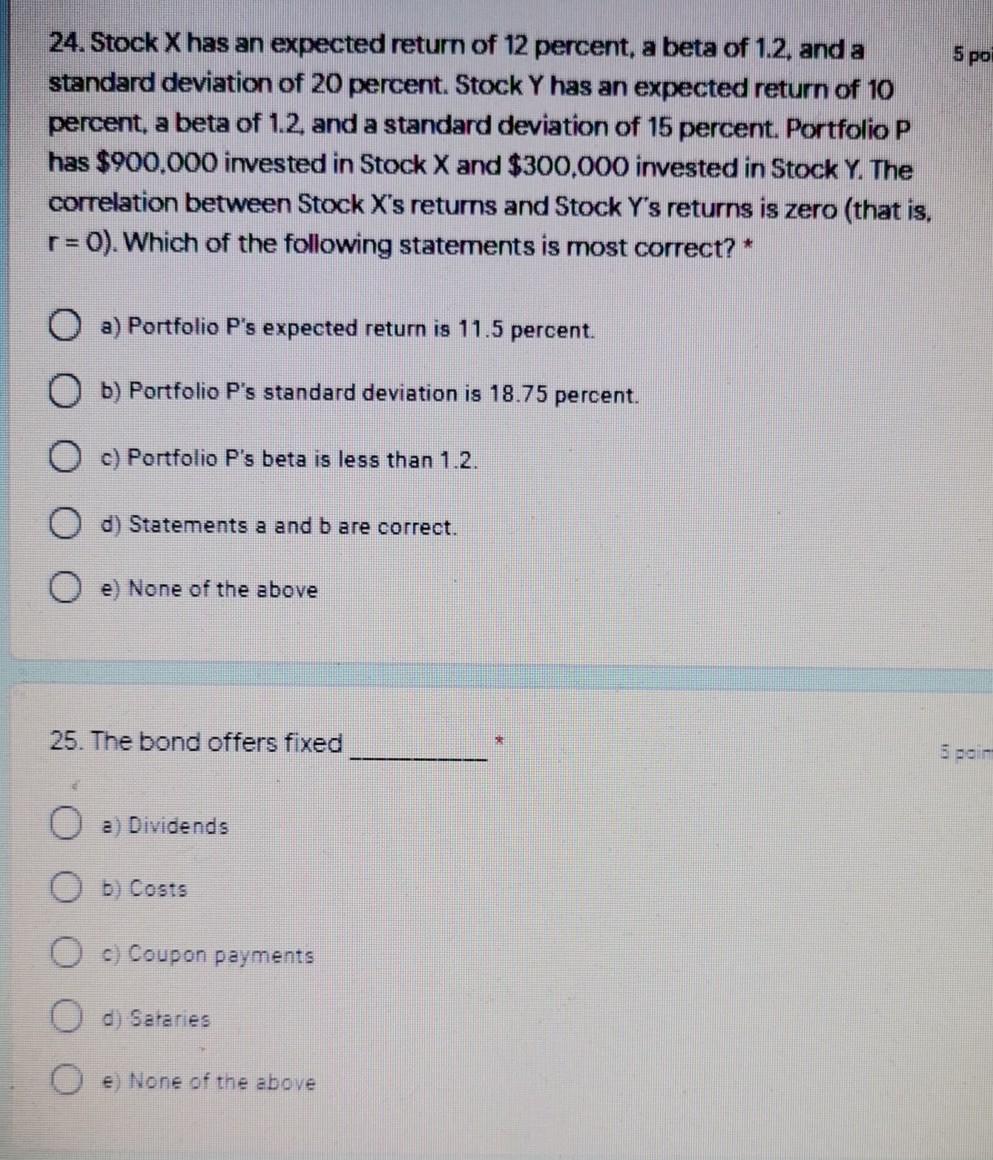

22. Pistaj Fund has purchased a bond with 17 years remaining until 2 po maturity and a $1,000 face value. The bond is currently selling at a price of $1,050. The bond offers 11% coupon rate with interest paid annually. The bond may be called in 5 years at a call price of $1,070. What is the bond's yield to call (YTC)? * O a. 15.11% O b. 13% O c. 17.5% O d. 10% O e None of the above 23. You are considering an investment in Tata's stock. which is expected to 2001- pay a dividend of $5.50 a share at the end of the year (D1 = $5.50) and has a beta of 0.9. The risk-free rate is 5.6%, and the market risk premium is 6%. Tata currently sells for $30.00 a share, and its dividend is expected to grow at some constant rate g. Assuming the market is in equilibrium, what does the market believe will be the stock price at the end of 3 years? a) $32.32 O b) 578.00 O c) $27 32 O c) So O e) None of the above 5 poi 24. Stock X has an expected return of 12 percent, a beta of 1.2, and a standard deviation of 20 percent. Stock Y has an expected return of 10 percent, a beta of 1.2. and a standard deviation of 15 percent. Portfolio P has $900.000 invested in Stock X and $300,000 invested in Stock Y. The correlation between Stock X's returns and Stock Y's returns is zero (that is, r = 0). Which of the following statements is most correct? O a) Portfolio P's expected return is 11.5 percent. O b) Portfolio P's standard deviation is 18.75 percent. c) Portfolio P's beta is less than 1.2. d) Statements a and b are correct. e) None of the above 25. The bond offers fixed e) Dividends b) Costs c) Coupon payments d) Sataries O e) None of the above

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started