Question

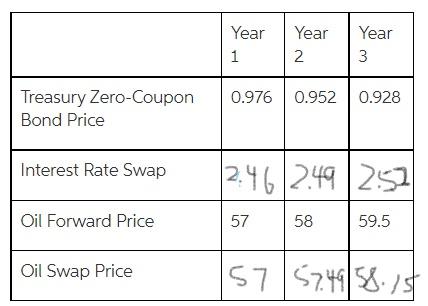

2.46 2.49 2.52 57 57.49 58.15 1a.Consider the 3-year oil swap. 2 years later, the oil price is $57/barrel. If cash settlement occurs, how much

2.46 2.49 2.52

57 57.49 58.15

1a.Consider the 3-year oil swap. 2 years later, the oil price is $57/barrel. If cash settlement occurs, how much is the payment (negative sign for receipt) of the floating price payer in year 2 on a 1,000-barrel swap agreement? (Leave your answers in 2 d.p.)

b

Consider the 3-year oil swap. Suppose a dealer is paying the fixed price and receiving floating. What position in oil forward contracts will hedge oil price risk in this position?

Long 1-year, 2-year and 3-year forwards.

Short 1-year, 2-year and 3-year forwards.

Short 1-year, 2-year forwards.

Long 1-year, 2-year forwards. Short 3-year forward.

c What is the swap price of a 2-year oil swap with the first settlement occurring in Year 2?

d What is the price of a 3-year swap for which two barrels of oil are delivered in Year 1 and 3 and one barrel of oil in Year 2?

Year 1 Year 2 Year 3 0.976 0.9520.928 Treasury Zero-Coupon Bond Price Interest Rate Swap 12:46 2.49 2.52 / Oil Forward Price 57 58 59.5 Oil Swap Price 157 57.4958.15

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Market Takers Edge Insider Strategies From The Options Trading Floor

Authors: Dan Passarelli

1st Edition

007175492X,0071754946