Answered step by step

Verified Expert Solution

Question

1 Approved Answer

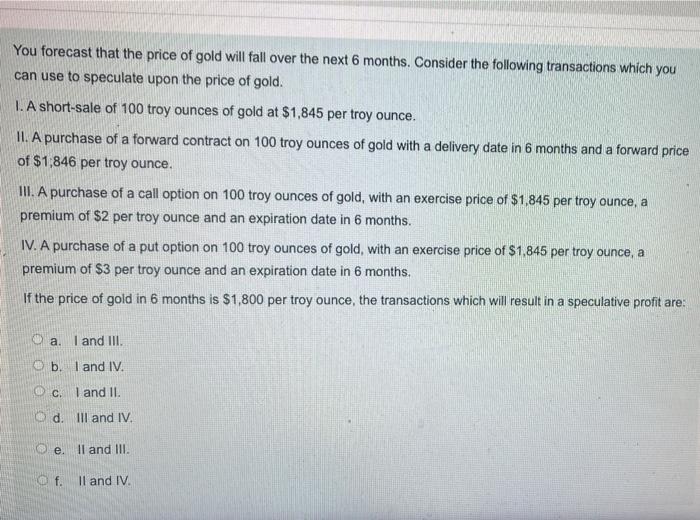

25 You forecast that the price of gold will fall over the next 6 months. Consider the following transactions which you can use to speculate

25

You forecast that the price of gold will fall over the next 6 months. Consider the following transactions which you can use to speculate upon the price of gold. 1. A short-sale of 100 troy ounces of gold at $1,845 per troy ounce. H. A purchase of a forward contract on 100 troy ounces of gold with a delivery date in 6 months and a forward price of $1,846 per troy ounce. III. A purchase of a call option on 100 troy ounces of gold, with an exercise price of $1,845 per troy ounce, a premium of $2 per troy ounce and an expiration date in 6 months. IV. A purchase of a put option on 100 troy ounces of gold, with an exercise price of $1,845 per troy ounce, a premium of $3 per troy ounce and an expiration date in 6 months. If the price of gold in 6 months is $1,800 per troy ounce, the transactions which will result in a speculative profit are: a. I and III. eb. I and IV. @c. I and II. 1 d. III and IV. e. II and III. @f. II and IV Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Household Finance Adrift In A Sea Of Red Ink Palgrave Macmillan Studies In Banking And Financial Institutions

Authors: D. Chorafas

1st Edition

1137299444, 1137299452, 9781137299451