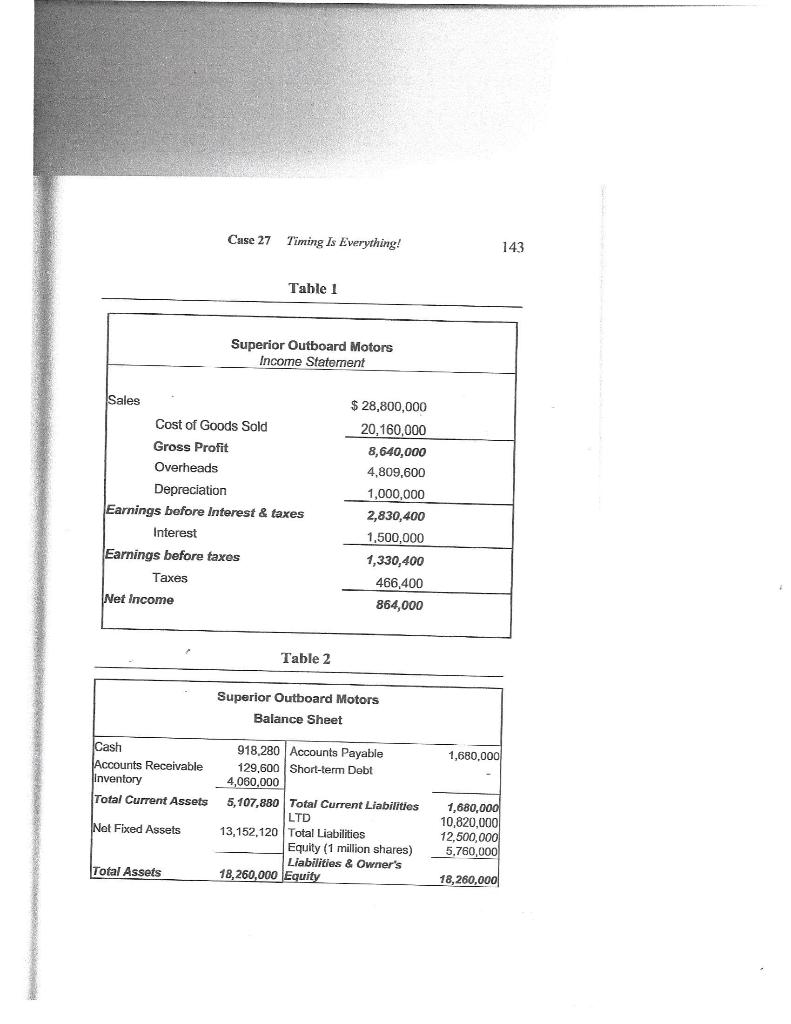

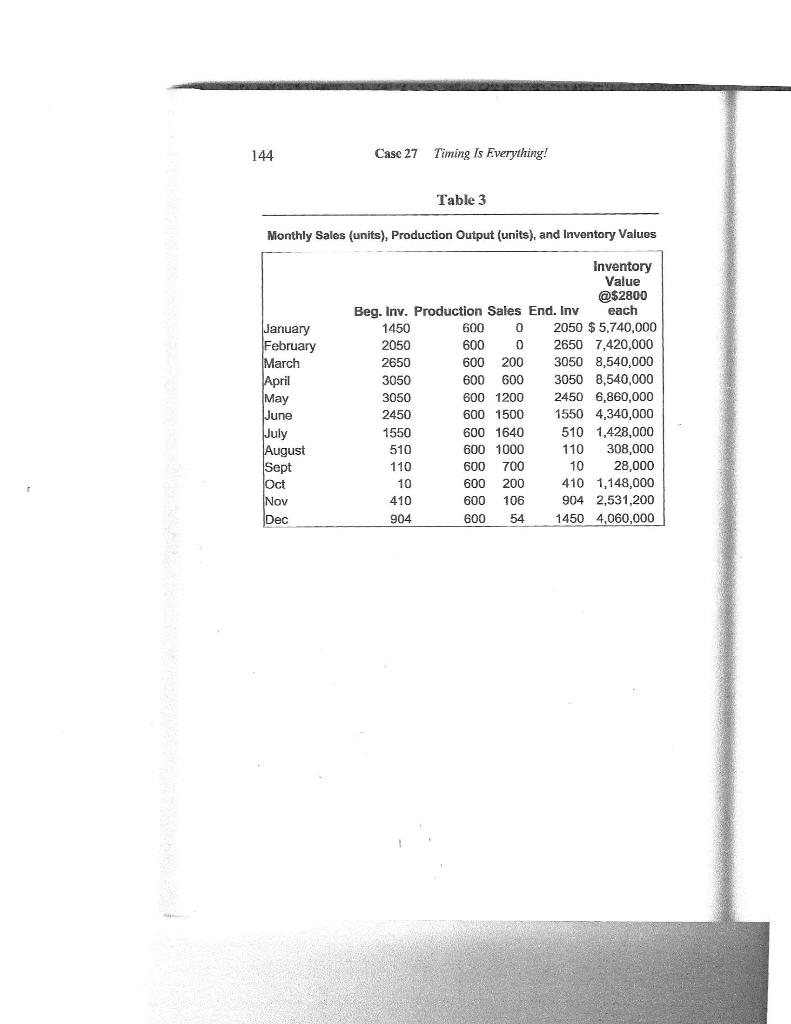

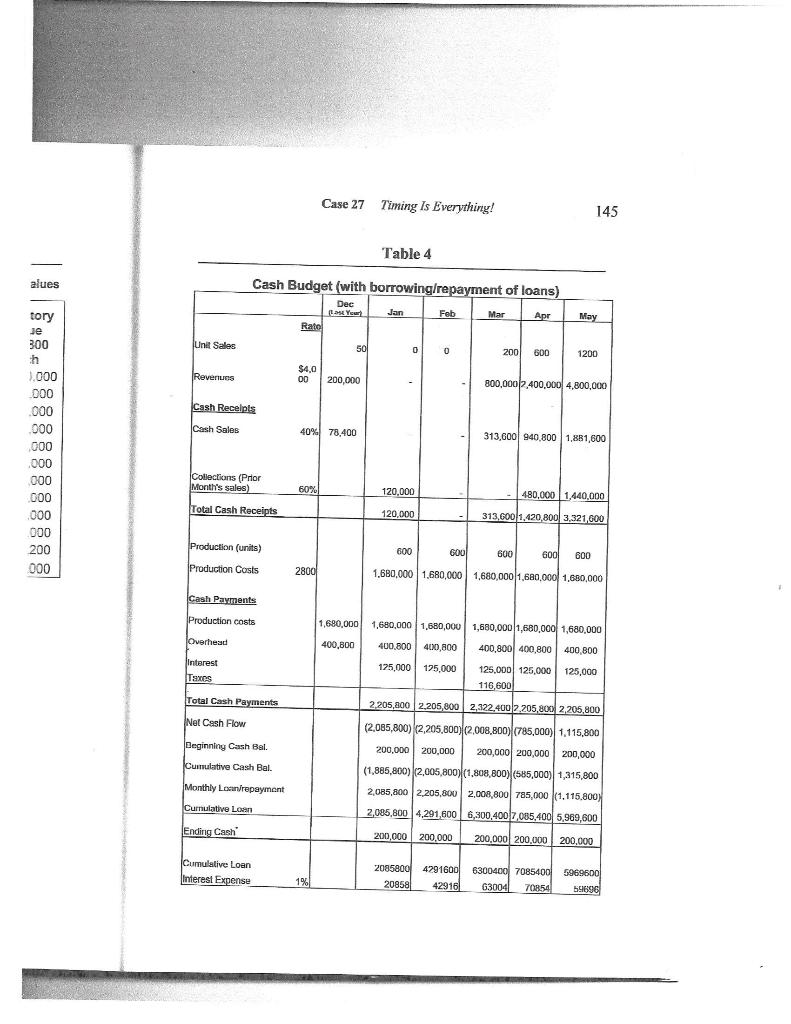

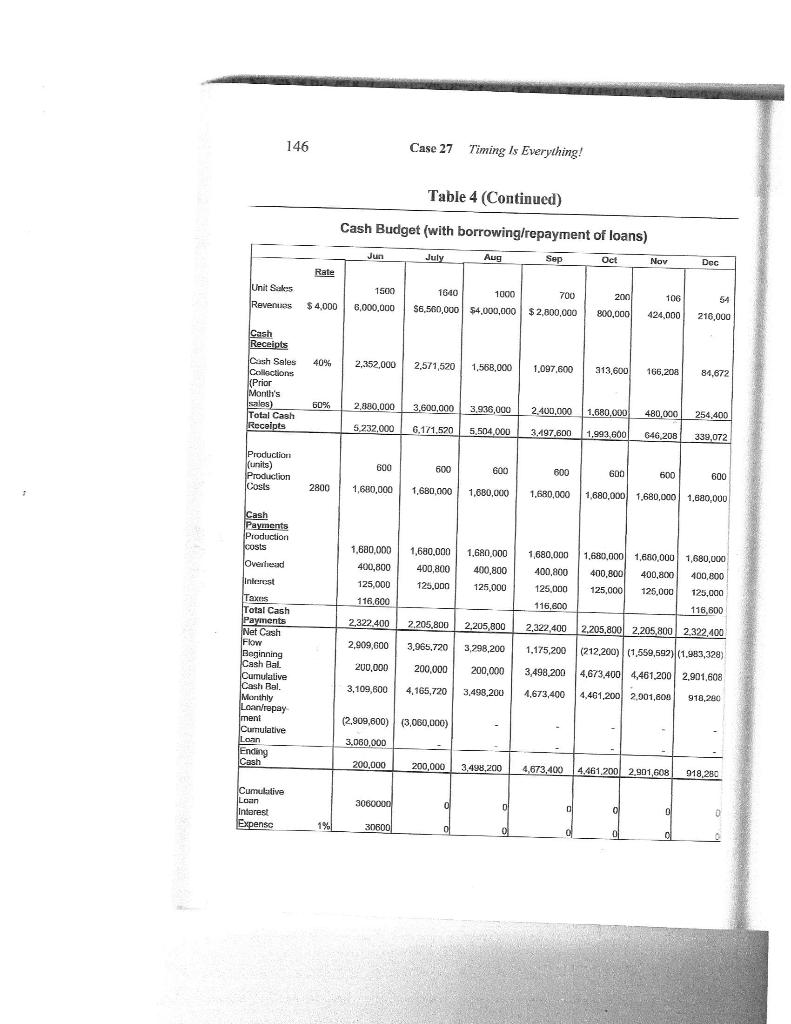

27 Working Capital Management Timing is Everything! "We have done it again," said George Brash, the president and chief executive officer of Superior Outboard Motors, to his group of senior inanagers at their January meeting. "Our sales for this past year are up over 8% compared to the previous year, but our net profit margin and earnings per share are down! The shareholders are understandably upset and are demanding answers. It won't be long before the analysts change their recommendations. We better come up with some explanations and strategies to rectify the problem." Superior Outboard Motors, headquartered in Tampa, Florida, had manufacturing facilities in Blaine, Washington and Elkhart, Indiana. It specialized in the manufacture of outboard motors of various capacitics, for small to mediuin sized boats. The average selling price of its motors was $4000 and the cost of production was $2800 per unit. The company had been in business for over 10 years and was well respected in the industry Case 27 Timing Is Everything! 141 In particular, analysts had rated its after-sales service, consumer relations, and treatment of employees pretty high in comparison with its competitors. The company's stock (SOMI), which traded in the over the counter market, had appreciated significantly up until the first quarter of the current year. After that, however, the company had reported a drop in EPS for three quarters in a row causing the stock price to go down and the shareholders to make frantic calls to the consumer relations office. "I think I know what the problem is, George," said Matt Snow, the vice-president of finance. "I have taken a look at our financial statements (sce Tables 1 and 2) and inventory figures for last year (see Table 3). While most of the expenses seem to be reasonable, I strongly believe that the policy of level monthly production, which was implemented at the start of the year, is main culprit. Ours is a seasonal business with the peak season being during the months of May- August. Yet, we seem to be maintaining a level production rate of 600 motors per month. As a result, our inventory builds up significantly during the lean months and sits there tying up our capital. With interest rates as high as they have been on our short-lerm borrowing (prime rate plus 3%, i.e. 9% plus 3%), the interest charges have been killing our profits. "As you can see in this cash budget that I have prepared (Table 4), our short-term debt varied between $2.09 million and $7.09 million during the first six months of the year. We ended the year with no short- term debt, but ended up paying almost $290,000 in interest expenses for the year. That's money that was spent primarily to finance inventory, which I might add, sat around for a few months. I recommend that we drop the level production policy and align our monthly production output with the forecasted sales for the month. I haven't worked out all the numbers yet, but I am quite sure that we will be able to boost our earnings quite a bit by making that change." "Wait a minute," said Mike Cooper, the production manager, from the other side of the room. "Have you considered the effect of that change on our workforce and employee morale? We will have to lay off people during lean times and scramble to hire more workers during peak production periods. That will have a negative effect on our operating efficiency and will result in some additional costs for training and orientation. My staff and I are in contact with these folks on a daily basis. I would hate to have to tell some of these 'nice' folks that they dent and group of year are argin and bly upset s change tions and rida, had diana. It apacities, s motors company d in the 142 Case 27 Timing Is Everything! were being laid off for a few months, especially when our annual sales have been going up. There's got to be a better way!" "Gentlemen," said George Brash, sensing that that the arguments were getting rather heated. "Let's not jump to any conclusions here. I think you both have expressed valid points. On the one hand, we can't lose sight of the fact that we value our employees and must continue caring for them. Yet on the other, we have a responsibility to our sharcholders. We cannot let our earnings and stock price keep on dropping, especially considering the fact that our sales have been going up on a consistent basis. As you all know, the market can be merciless, once the analysts change their tone. Matt, why don't you do the necessary number crunching and present the results at our next meeting. Let's analyze all aspects of our working capital management policies and try and come up with the best possible alternative. I think this experience clearly proves that in our business, as in most businesses, Timing is everything!" Case 27 Timing Is Everything! 143 Table 1 Superior Outboard Motors Income Statement Sales Cost of Goods Sold Gross Profit Overheads Depreciation Earnings before Interest & taxes Interest Earnings before taxes Taxes Net Income $ 28,800,000 20,160,000 8,640,000 4,809,600 1,000,000 2,830,400 1,500,000 1,330,400 466,400 864,000 Table 2 Superior Outboard Motors Balance Sheet 1,680,000 Cash Accounts Receivable Jinventory Total Current Assets 918.280 Accounts Payable 129,600 Short-term Debt 4,060,000 5,107,880 Total Current Liabilities LTD 13,152,120 Total Liabilities Equity (1 million shares) Liabilities & Owner's 18,260,000 Equity Net Fixed Assets 1,680,000 10,820,0001 12,500,000 5.760,000 Total Assets 18,260,000 144 Case 27 Timing Is Everything! Table 3 Monthly Sales (units), Production Output (units), and Inventory Values January February March April May June July August Sept loct Nov Dec Inventory Value @$2800 Beg. Inv. Production Sales End. Inv each 1450 600 0 2050 $ 5.740,000 2050 600 0 2650 7,420,000 2650 600 200 3050 8,540,000 3050 600 600 3050 8,540,000 3050 600 1200 2450 6,860,000 2450 600 1500 1550 4,340,000 1550 600 1640 510 1,428,000 510 600 1000 110 308,000 110 600 700 10 28,000 10 600 200 410 1,148,000 410 600 106 904 2,531,200 904 600 54 1450 4,060,000 ! Case 27 Timing Is Everything! 145 Table 4 alues Cash Budget (with borrowing/repayment of loans) Dec 12 Year Jan Feb Mar Apr May Rate Unit Sales 50 01 0 200 600 1200 Revenues $4.0 00 200,000 800,000 2,400,000 4,800,000 Cash Recepts Cash Sales 40% 78,400 313,600 940,800 1,881,600 tory je 300 h 1,000 000 .000 000 000 000 000 .000 000 000 200 000 Collections (Prior Month's sales) 60% 120,000 480,000 1,440,000 Total Cash Receipts 120,000 313,600 1,420 800 3,321,600 Production (units) 600 600 600 600 800 Production Costs 2800 1.680,000 1.680,000 1,680,000 1,680,000 1,680,000 Cash Payments Production costs Overhead 1,680,000 1,680,000 1,680,000 1,680,000 1,680,000 1,680,000 400,800 400.800 400,000 400,800 400,800 400 800 125,000 125.000 125.000 125.000 125,000 116,600 Interest Taxes Total Cash Payments 2.205,000 2.205,800 2,322,400 2.205,800 2,205,800 Net Cash Flow (2,085,800) 2,205,800)|(2,008,800)|(785,000) 1,115,800 Beginning Cash Bal. 200.000 200.000 200.000 200.000 200.000 Cumulative Cash Bal. Monthly Loun/repayment (1,885,800)|(2,005,800)|(1,808,800)|(585,000) 1,315,800 2,085,800 2,205,800 2,008,800 785,000 (1,115,800) 2,085,800 4,291,600 6,300,400 7,085,400 5,969,600 Cumulative Loan Ending Cash 200.000 200.000 200.000 200.000 200,000 Cumulative Loan Interest Expense 1% 2085800 4291600 20858 42916 63004007085400 63004 70854 5969600 59696 146 Case 27 Timing Is Everything! ! Table 4 (Continued) Cash Budget (with borrowing/repayment of loans) Jun July Aug Sep Oct Nov Dec Rate Unit Seks 1500 106 54 Revenues $ 4,000 6.000.000 1640 1000 700 $6,500,000 $4,000,000 $2,800,000 200 800,000 424,000 216,000 40% 2,352,000 2.571,520 1,568,000 1,097,600 313,600 166,208 84,672 Cash Receipts Cash Sales Collections (Prior Month's sales) Total Cash Recolots 60% 2.880,000 3,600,000 3,936,000 2.400.000 1,680,000 480,000 254,400 5.232,000 6.171.520 5,504,000 3.197,600 1,993.600 646,208 339,072 Production (units) Production Costs 600 600 600 600 600 600 600 600 2800 + 1,680,000 1,680.000 1,680,000 1,680,000 1,680,000 1,680,000 1,800.000 1,680,000 1,680,000 1,680,000 Cash Payments Production Costs Overhead Interest Taxes ITotal Cash Payments Net Cash Flow 1,680,000 400,800 125,000 400.800 400,800 125,000 125,000 400,800 125,000 116,600 1,680,000 1,880,000 1,680,000 400,800 400,800 400,800 125,000 125.000 125,000 116,600 116,600 2,322.400 2.205.800 2,205 800 2,322,400 2,205,800 2,205,800 2,322,400 2,909,600 Beginning 3,965,720 3,298,200 1,175,200 (212.200)|(1,559,592)|(1.583,328) 200,000 200,000 200,000 3,498,200 4,673.400 4,461.200 2.901,608 3,109,600 4,165,720 3,498,200 4.673,400 4,461,200 2,001,800 918,280 Cash Bal Cumulative Cash Bal. Monthly Loan/repay ment Cumulative Loan Ending Cash (2.909,600) (3,060,000) 3,060,000 200,000 200,000 3,498,209 4,673,400 4.461.200 2.901 608018,280 Cumulutive Loan Interest Expensc 3060000 0 0 0 0 1% 30600 0 DI Case 27 Timing Is Everything! 147 Questions: 1. Comment on Superior Outboard Motors' absolute and relative liquidity positions. 54 2. Examine the company's monthly inventory turnover ratio. What does it indicate? 005 572 3. How long are the firm's operating and cash cycles? Using a suitable diagram show the breakdown of the firm's operating cycle into its relevant components. What do your findings indicate? 00 4. How much higher would the firm's earnings per share have been if it had followed a policy of aligning the production output with the number of units sold each month? 00 5. Calculate the monthly net working capital figures for the company. Comment on your findings. 6. Is the firm following an aggressive or a conservative financing policy for funding its working capital? Explain. 7. Is Matt correct in stating that the main culprit is the firm's production policy? Besides changing the production levels per month, are there any other things that the firm can realistically do to boost earnings per share? 8. Using DuPont analysis, comment on the firm's profit situation. 9. Do you agree with the production manager's comment that that "there's got to be a better way"? Please explain. 27 Working Capital Management Timing is Everything! "We have done it again," said George Brash, the president and chief executive officer of Superior Outboard Motors, to his group of senior inanagers at their January meeting. "Our sales for this past year are up over 8% compared to the previous year, but our net profit margin and earnings per share are down! The shareholders are understandably upset and are demanding answers. It won't be long before the analysts change their recommendations. We better come up with some explanations and strategies to rectify the problem." Superior Outboard Motors, headquartered in Tampa, Florida, had manufacturing facilities in Blaine, Washington and Elkhart, Indiana. It specialized in the manufacture of outboard motors of various capacitics, for small to mediuin sized boats. The average selling price of its motors was $4000 and the cost of production was $2800 per unit. The company had been in business for over 10 years and was well respected in the industry Case 27 Timing Is Everything! 141 In particular, analysts had rated its after-sales service, consumer relations, and treatment of employees pretty high in comparison with its competitors. The company's stock (SOMI), which traded in the over the counter market, had appreciated significantly up until the first quarter of the current year. After that, however, the company had reported a drop in EPS for three quarters in a row causing the stock price to go down and the shareholders to make frantic calls to the consumer relations office. "I think I know what the problem is, George," said Matt Snow, the vice-president of finance. "I have taken a look at our financial statements (sce Tables 1 and 2) and inventory figures for last year (see Table 3). While most of the expenses seem to be reasonable, I strongly believe that the policy of level monthly production, which was implemented at the start of the year, is main culprit. Ours is a seasonal business with the peak season being during the months of May- August. Yet, we seem to be maintaining a level production rate of 600 motors per month. As a result, our inventory builds up significantly during the lean months and sits there tying up our capital. With interest rates as high as they have been on our short-lerm borrowing (prime rate plus 3%, i.e. 9% plus 3%), the interest charges have been killing our profits. "As you can see in this cash budget that I have prepared (Table 4), our short-term debt varied between $2.09 million and $7.09 million during the first six months of the year. We ended the year with no short- term debt, but ended up paying almost $290,000 in interest expenses for the year. That's money that was spent primarily to finance inventory, which I might add, sat around for a few months. I recommend that we drop the level production policy and align our monthly production output with the forecasted sales for the month. I haven't worked out all the numbers yet, but I am quite sure that we will be able to boost our earnings quite a bit by making that change." "Wait a minute," said Mike Cooper, the production manager, from the other side of the room. "Have you considered the effect of that change on our workforce and employee morale? We will have to lay off people during lean times and scramble to hire more workers during peak production periods. That will have a negative effect on our operating efficiency and will result in some additional costs for training and orientation. My staff and I are in contact with these folks on a daily basis. I would hate to have to tell some of these 'nice' folks that they dent and group of year are argin and bly upset s change tions and rida, had diana. It apacities, s motors company d in the 142 Case 27 Timing Is Everything! were being laid off for a few months, especially when our annual sales have been going up. There's got to be a better way!" "Gentlemen," said George Brash, sensing that that the arguments were getting rather heated. "Let's not jump to any conclusions here. I think you both have expressed valid points. On the one hand, we can't lose sight of the fact that we value our employees and must continue caring for them. Yet on the other, we have a responsibility to our sharcholders. We cannot let our earnings and stock price keep on dropping, especially considering the fact that our sales have been going up on a consistent basis. As you all know, the market can be merciless, once the analysts change their tone. Matt, why don't you do the necessary number crunching and present the results at our next meeting. Let's analyze all aspects of our working capital management policies and try and come up with the best possible alternative. I think this experience clearly proves that in our business, as in most businesses, Timing is everything!" Case 27 Timing Is Everything! 143 Table 1 Superior Outboard Motors Income Statement Sales Cost of Goods Sold Gross Profit Overheads Depreciation Earnings before Interest & taxes Interest Earnings before taxes Taxes Net Income $ 28,800,000 20,160,000 8,640,000 4,809,600 1,000,000 2,830,400 1,500,000 1,330,400 466,400 864,000 Table 2 Superior Outboard Motors Balance Sheet 1,680,000 Cash Accounts Receivable Jinventory Total Current Assets 918.280 Accounts Payable 129,600 Short-term Debt 4,060,000 5,107,880 Total Current Liabilities LTD 13,152,120 Total Liabilities Equity (1 million shares) Liabilities & Owner's 18,260,000 Equity Net Fixed Assets 1,680,000 10,820,0001 12,500,000 5.760,000 Total Assets 18,260,000 144 Case 27 Timing Is Everything! Table 3 Monthly Sales (units), Production Output (units), and Inventory Values January February March April May June July August Sept loct Nov Dec Inventory Value @$2800 Beg. Inv. Production Sales End. Inv each 1450 600 0 2050 $ 5.740,000 2050 600 0 2650 7,420,000 2650 600 200 3050 8,540,000 3050 600 600 3050 8,540,000 3050 600 1200 2450 6,860,000 2450 600 1500 1550 4,340,000 1550 600 1640 510 1,428,000 510 600 1000 110 308,000 110 600 700 10 28,000 10 600 200 410 1,148,000 410 600 106 904 2,531,200 904 600 54 1450 4,060,000 ! Case 27 Timing Is Everything! 145 Table 4 alues Cash Budget (with borrowing/repayment of loans) Dec 12 Year Jan Feb Mar Apr May Rate Unit Sales 50 01 0 200 600 1200 Revenues $4.0 00 200,000 800,000 2,400,000 4,800,000 Cash Recepts Cash Sales 40% 78,400 313,600 940,800 1,881,600 tory je 300 h 1,000 000 .000 000 000 000 000 .000 000 000 200 000 Collections (Prior Month's sales) 60% 120,000 480,000 1,440,000 Total Cash Receipts 120,000 313,600 1,420 800 3,321,600 Production (units) 600 600 600 600 800 Production Costs 2800 1.680,000 1.680,000 1,680,000 1,680,000 1,680,000 Cash Payments Production costs Overhead 1,680,000 1,680,000 1,680,000 1,680,000 1,680,000 1,680,000 400,800 400.800 400,000 400,800 400,800 400 800 125,000 125.000 125.000 125.000 125,000 116,600 Interest Taxes Total Cash Payments 2.205,000 2.205,800 2,322,400 2.205,800 2,205,800 Net Cash Flow (2,085,800) 2,205,800)|(2,008,800)|(785,000) 1,115,800 Beginning Cash Bal. 200.000 200.000 200.000 200.000 200.000 Cumulative Cash Bal. Monthly Loun/repayment (1,885,800)|(2,005,800)|(1,808,800)|(585,000) 1,315,800 2,085,800 2,205,800 2,008,800 785,000 (1,115,800) 2,085,800 4,291,600 6,300,400 7,085,400 5,969,600 Cumulative Loan Ending Cash 200.000 200.000 200.000 200.000 200,000 Cumulative Loan Interest Expense 1% 2085800 4291600 20858 42916 63004007085400 63004 70854 5969600 59696 146 Case 27 Timing Is Everything! ! Table 4 (Continued) Cash Budget (with borrowing/repayment of loans) Jun July Aug Sep Oct Nov Dec Rate Unit Seks 1500 106 54 Revenues $ 4,000 6.000.000 1640 1000 700 $6,500,000 $4,000,000 $2,800,000 200 800,000 424,000 216,000 40% 2,352,000 2.571,520 1,568,000 1,097,600 313,600 166,208 84,672 Cash Receipts Cash Sales Collections (Prior Month's sales) Total Cash Recolots 60% 2.880,000 3,600,000 3,936,000 2.400.000 1,680,000 480,000 254,400 5.232,000 6.171.520 5,504,000 3.197,600 1,993.600 646,208 339,072 Production (units) Production Costs 600 600 600 600 600 600 600 600 2800 + 1,680,000 1,680.000 1,680,000 1,680,000 1,680,000 1,680,000 1,800.000 1,680,000 1,680,000 1,680,000 Cash Payments Production Costs Overhead Interest Taxes ITotal Cash Payments Net Cash Flow 1,680,000 400,800 125,000 400.800 400,800 125,000 125,000 400,800 125,000 116,600 1,680,000 1,880,000 1,680,000 400,800 400,800 400,800 125,000 125.000 125,000 116,600 116,600 2,322.400 2.205.800 2,205 800 2,322,400 2,205,800 2,205,800 2,322,400 2,909,600 Beginning 3,965,720 3,298,200 1,175,200 (212.200)|(1,559,592)|(1.583,328) 200,000 200,000 200,000 3,498,200 4,673.400 4,461.200 2.901,608 3,109,600 4,165,720 3,498,200 4.673,400 4,461,200 2,001,800 918,280 Cash Bal Cumulative Cash Bal. Monthly Loan/repay ment Cumulative Loan Ending Cash (2.909,600) (3,060,000) 3,060,000 200,000 200,000 3,498,209 4,673,400 4.461.200 2.901 608018,280 Cumulutive Loan Interest Expensc 3060000 0 0 0 0 1% 30600 0 DI Case 27 Timing Is Everything! 147 Questions: 1. Comment on Superior Outboard Motors' absolute and relative liquidity positions. 54 2. Examine the company's monthly inventory turnover ratio. What does it indicate? 005 572 3. How long are the firm's operating and cash cycles? Using a suitable diagram show the breakdown of the firm's operating cycle into its relevant components. What do your findings indicate? 00 4. How much higher would the firm's earnings per share have been if it had followed a policy of aligning the production output with the number of units sold each month? 00 5. Calculate the monthly net working capital figures for the company. Comment on your findings. 6. Is the firm following an aggressive or a conservative financing policy for funding its working capital? Explain. 7. Is Matt correct in stating that the main culprit is the firm's production policy? Besides changing the production levels per month, are there any other things that the firm can realistically do to boost earnings per share? 8. Using DuPont analysis, comment on the firm's profit situation. 9. Do you agree with the production manager's comment that that "there's got to be a better way"? Please explain