Answered step by step

Verified Expert Solution

Question

1 Approved Answer

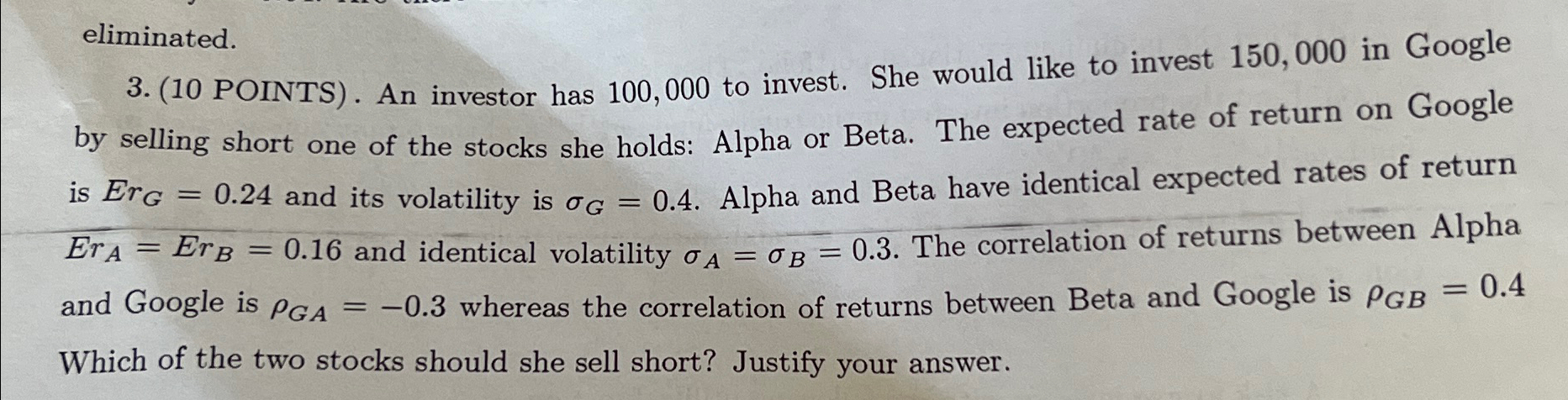

3 . ( 1 0 POINTS ) . An investor has 1 0 0 , 0 0 0 to invest. She would like to invest

POINTS An investor has to invest. She would like to invest in Google by selling short one of the stocks she holds: Alpha or Beta. The expected rate of return on Google is and its volatility is Alpha and Beta have identical expected rates of return and identical volatility The correlation of returns between Alpha and Google is whereas the correlation of returns between Beta and Google is Which of the two stocks should she sell short? Justify your answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Decentralized Finance How DeFi Is Changing The Future Of Money

Authors: Rhian Lewis

1st Edition

1398609390, 978-1398609396