Answered step by step

Verified Expert Solution

Question

1 Approved Answer

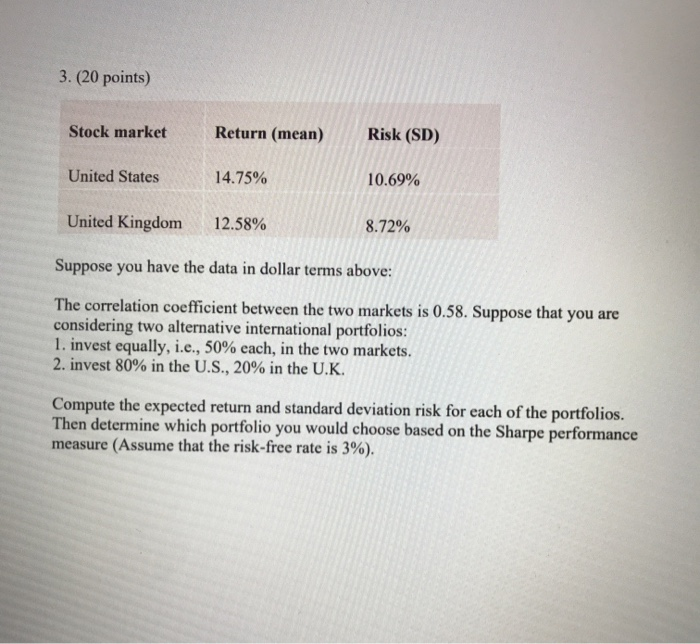

3. (20 points) Stock market Return (mean) Risk (SD) United States 14.75% 10.69% United Kingdom 12.58% 8.72% Suppose you have the data in dollar terms

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Totem Asset Group A Collection Of Market Essays June 2014 September 2018

Authors: Andrew C Strasman

1st Edition

0997987804, 978-0997987805