Answered step by step

Verified Expert Solution

Question

1 Approved Answer

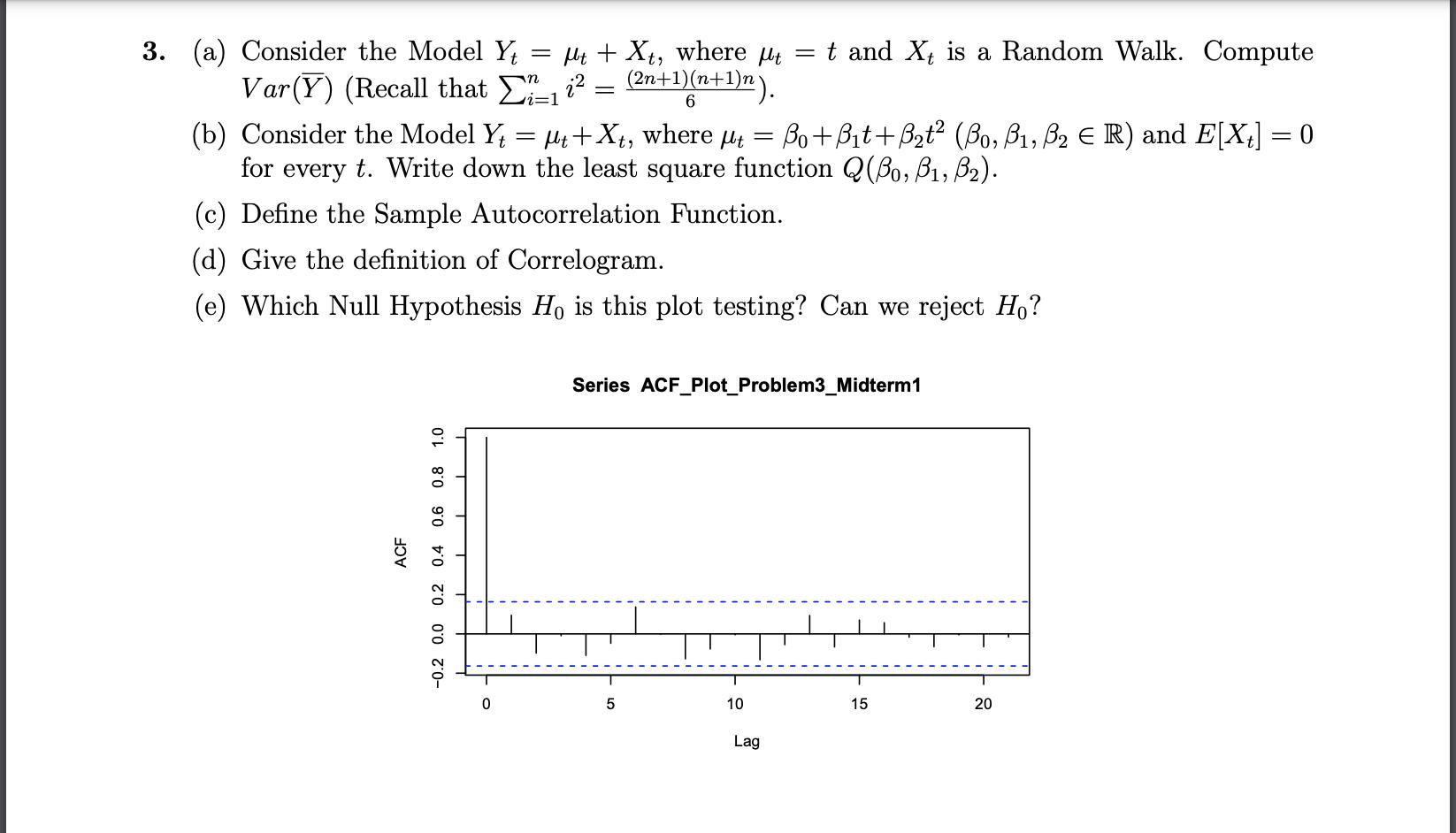

3. (a) Consider the Model Yt = Mt + Xt where Var(Y) (Recall that i = (n+1)(n+1)n). (b) Consider the Model Y = Mt+Xt,

3. (a) Consider the Model Yt = Mt + Xt where Var(Y) (Recall that i = (n+1)(n+1)n). (b) Consider the Model Y = Mt+Xt, where = Bo+Bt+Bt (Bo, B, B R) and E[Xt] = 0 for every t. Write down the least square function Q(Bo, B, B). (c) Define the Sample Autocorrelation Function. (d) Give the definition of Correlogram. (e) Which Null Hypothesis Ho is this plot testing? Can we reject Ho? ACF 1.0 0.6 0.8 -0.2 0.0 0.2 0.4 0 ft = t and X is a Random Walk. Compute Series ACF_Plot_Problem3_Midterm 1 5 10 Lag 15 20

Step by Step Solution

★★★★★

3.45 Rating (165 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Econometrics

Authors: James H. Stock, Mark W. Watson

3rd edition

133595420, 978-0138009007, 138009007, 978-0133486872, 133486877, 978-0133595420