Answered step by step

Verified Expert Solution

Question

1 Approved Answer

3. (a) You have a two year riskless bond which pays an annual coupon of 3% each year and then finally returns the full principal

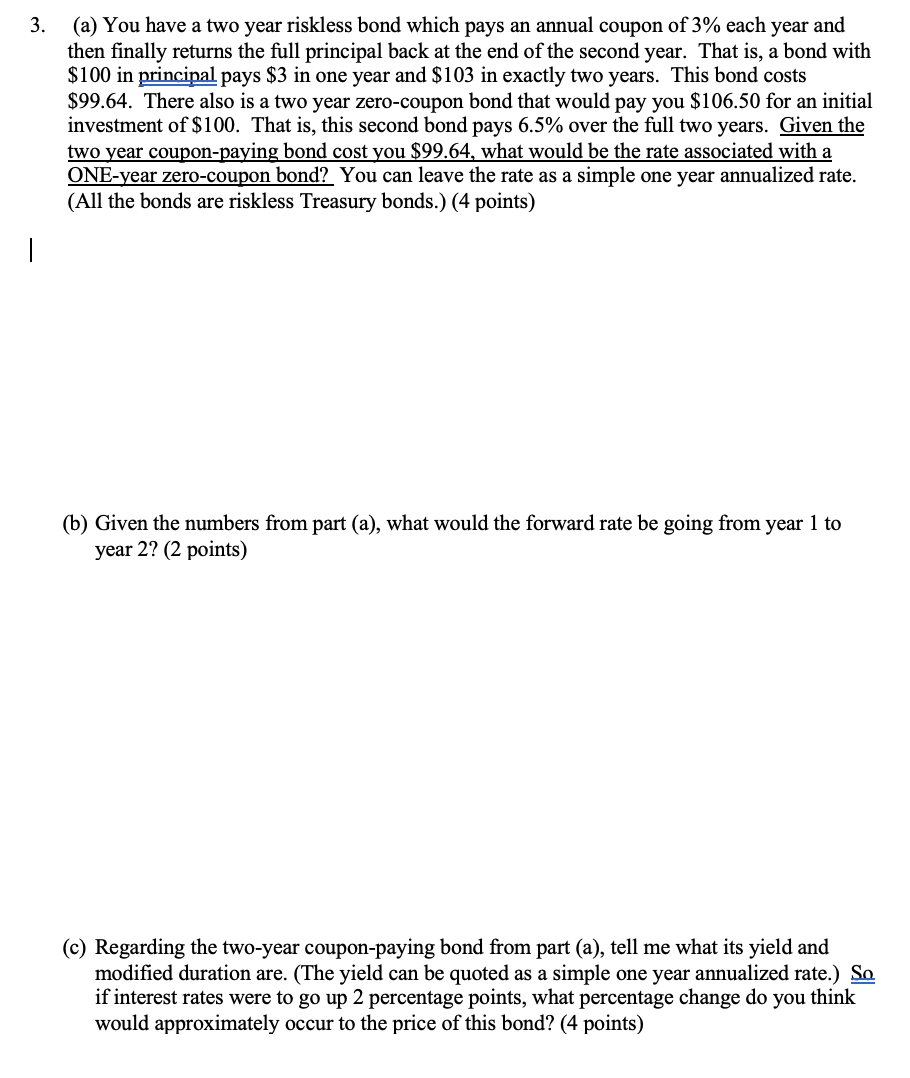

3. (a) You have a two year riskless bond which pays an annual coupon of 3% each year and then finally returns the full principal back at the end of the second year. That is, a bond with $100 in principal pays $3 in one year and $103 in exactly two years. This bond costs $99.64. There also is a two year zero-coupon bond that would pay you $106.50 for an initial investment of $100. That is, this second bond pays 6.5% over the full two years. Given the two year coupon-paying bond cost you $99.64, what would be the rate associated with a ONE-year zero-coupon bond? You can leave the rate as a simple one year annualized rate. (All the bonds are riskless Treasury bonds.) (4 points) (b) Given the numbers from part (a), what would the forward rate be going from year 1 to year 2 ? ( 2 points) (c) Regarding the two-year coupon-paying bond from part (a), tell me what its yield and modified duration are. (The yield can be quoted as a simple one year annualized rate.) So if interest rates were to go up 2 percentage points, what percentage change do you think would approximately occur to the price of this bond? (4 points)

3. (a) You have a two year riskless bond which pays an annual coupon of 3% each year and then finally returns the full principal back at the end of the second year. That is, a bond with $100 in principal pays $3 in one year and $103 in exactly two years. This bond costs $99.64. There also is a two year zero-coupon bond that would pay you $106.50 for an initial investment of $100. That is, this second bond pays 6.5% over the full two years. Given the two year coupon-paying bond cost you $99.64, what would be the rate associated with a ONE-year zero-coupon bond? You can leave the rate as a simple one year annualized rate. (All the bonds are riskless Treasury bonds.) (4 points) (b) Given the numbers from part (a), what would the forward rate be going from year 1 to year 2 ? ( 2 points) (c) Regarding the two-year coupon-paying bond from part (a), tell me what its yield and modified duration are. (The yield can be quoted as a simple one year annualized rate.) So if interest rates were to go up 2 percentage points, what percentage change do you think would approximately occur to the price of this bond? (4 points) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Islamic Finance

Authors: Karen Hunt-Ahmed

1st Edition

1118180909, 978-1118180907