Answered step by step

Verified Expert Solution

Question

1 Approved Answer

3. An investor owns a stock. Daily change in stock price, AS, has the standard deviation of 10. To hedge risks of the stock

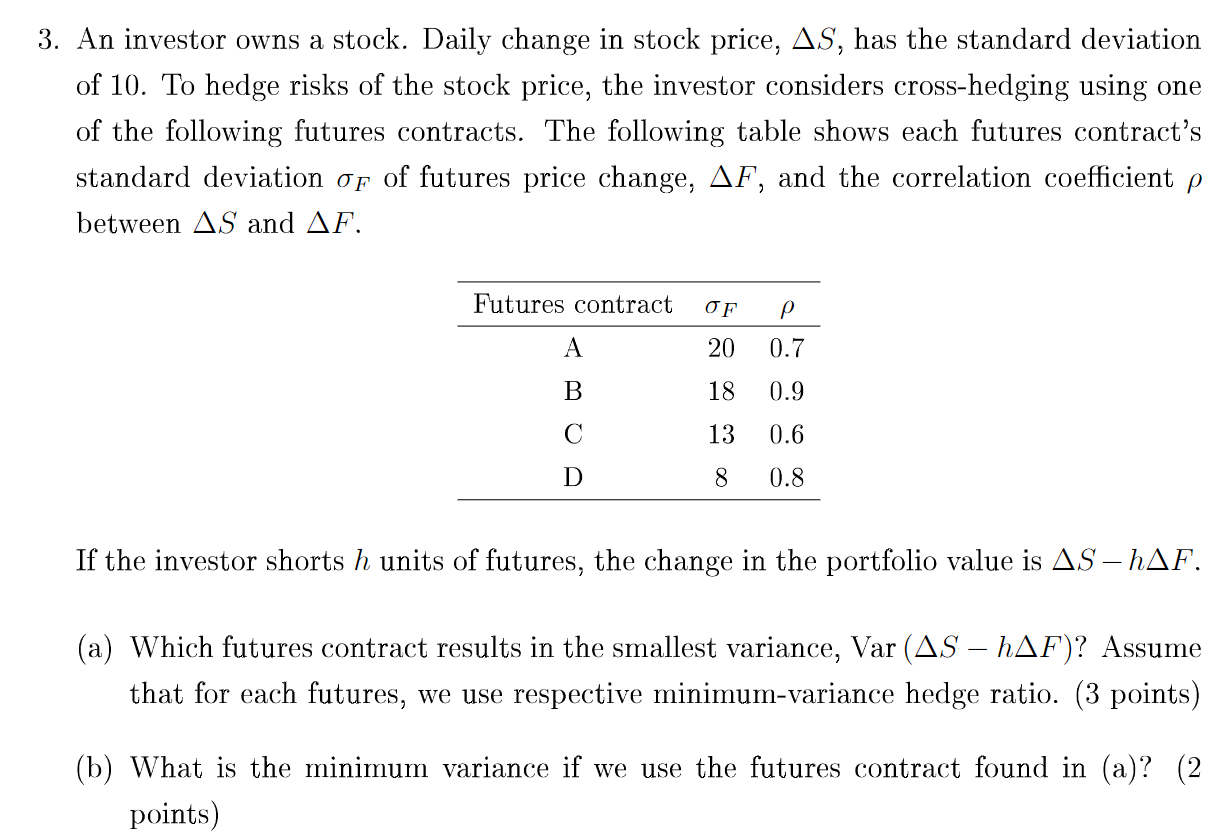

3. An investor owns a stock. Daily change in stock price, AS, has the standard deviation of 10. To hedge risks of the stock price, the investor considers cross-hedging using one of the following futures contracts. The following table shows each futures contract's standard deviation of of futures price change, AF, and the correlation coefficient p between AS and AF. Futures contract OF P 20 0.7 18 0.9 13 0.6 8 0.8 A B D If the investor shorts h units of futures, the change in the portfolio value is AS - hAF. (a) Which futures contract results in the smallest variance, Var (AS hAF)? Assume that for each futures, we use respective minimum-variance hedge ratio. (3 points) (b) What is the minimum variance if we use the futures contract found in (a)? (2 points)

Step by Step Solution

★★★★★

3.39 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

To determine the futures contract that results in the smallest variance we need to calculate the min...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management A Risk Management Approach

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders

8th edition

978-0078034800, 78034809, 978-0071051590