Answered step by step

Verified Expert Solution

Question

1 Approved Answer

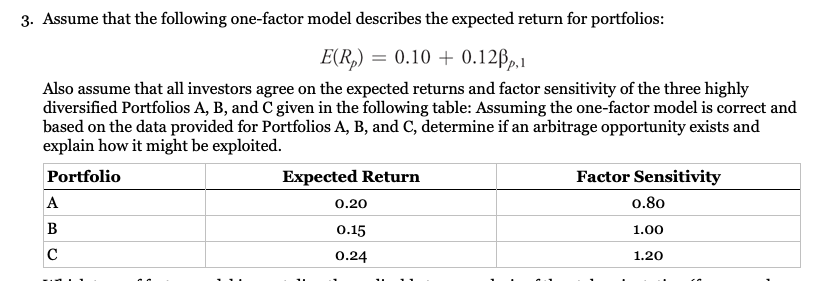

3. Assume that the following one-factor model describes the expected return for portfolios: E(R) 0.10 +0.12p,1 Also assume that all investors agree on the

3. Assume that the following one-factor model describes the expected return for portfolios: E(R) 0.10 +0.12p,1 Also assume that all investors agree on the expected returns and factor sensitivity of the three highly diversified Portfolios A, B, and C given in the following table: Assuming the one-factor model is correct and based on the data provided for Portfolios A, B, and C, determine if an arbitrage opportunity exists and explain how it might be exploited. Portfolio A B C Expected Return 0.20 0.15 0.24 Factor Sensitivity 0.80 1.00 1.20

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Matlab An Introduction with Applications

Authors: Amos Gilat

5th edition

1118629868, 978-1118801802, 1118801806, 978-1118629864