Answered step by step

Verified Expert Solution

Question

1 Approved Answer

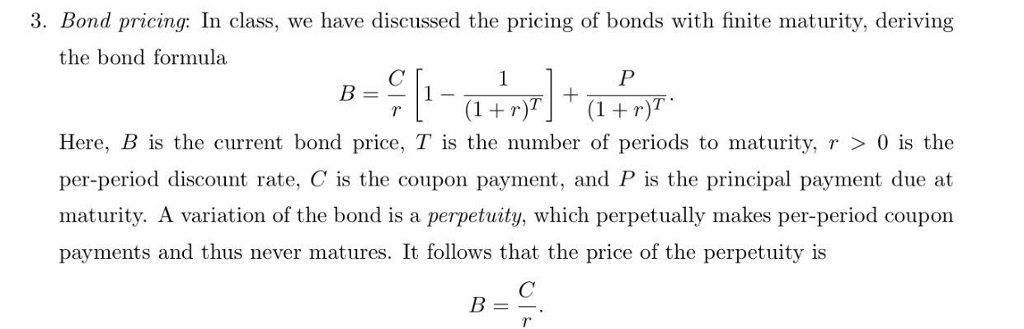

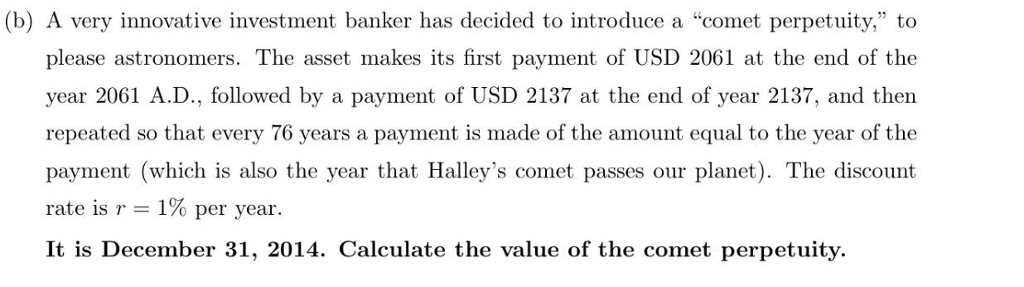

3. Bond pricing: In class, we have discussed the pricing of bonds with finite maturity, deriving the bond formula (1 +r) (1 r) Here, B

3. Bond pricing: In class, we have discussed the pricing of bonds with finite maturity, deriving the bond formula (1 +r) (1 r) Here, B is the current bond price, T is the number of periods to maturity, r 0 is the per-period discount rate, C is the coupon payment, and P is the principal payment due at maturity. A variation of the bond is a perpetuity, which perpetually makes per-period coupon payments and thus never matures. It follows that the price of the perpetuity is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supernatural Provision Living In Financial Freedom

Authors: Joan Hunter, Sid Roth

1st Edition

1641238232, 978-1641238236