Answered step by step

Verified Expert Solution

Question

1 Approved Answer

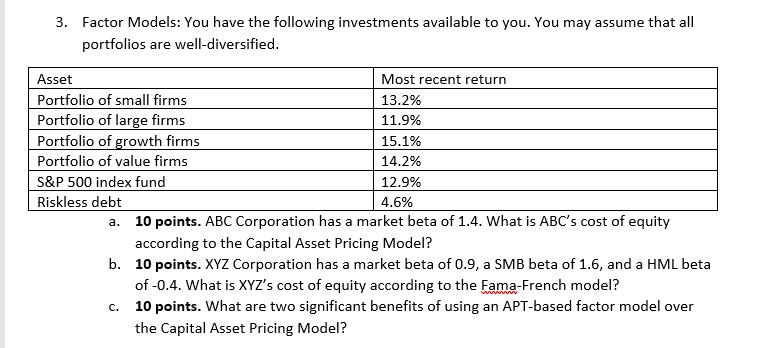

3. Factor Models: You have the following investments available to you. You may assume that all portfolios are well-diversified. Asset Portfolio of small firms

3. Factor Models: You have the following investments available to you. You may assume that all portfolios are well-diversified. Asset Portfolio of small firms Portfolio of large firms Portfolio of growth firms Portfolio of value firms Most recent return 13.2% 11.9% 15.1% 14.2% 12.9% 4.6% a. 10 points. ABC Corporation has a market beta of 1.4. What is ABC's cost of equity according to the Capital Asset Pricing Model? S&P 500 index fund Riskless debt b. 10 points. XYZ Corporation has a market beta of 0.9, a SMB beta of 1.6, and a HML beta of -0.4. What is XYZ's cost of equity according to the Fama-French model? c. 10 points. What are two significant benefits of using an APT-based factor model over the Capital Asset Pricing Model?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Eugene F. Brigham, Phillip R. Daves

11th edition

978-1111530266