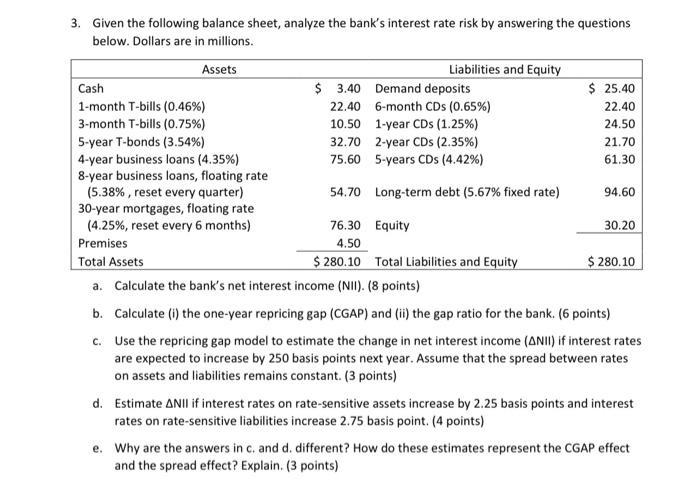

3. Given the following balance sheet, analyze the bank's interest rate risk by answering the questions below. Dollars are in millions Assets Liabilities and Equity Cash $ 3.40 Demand deposits $ 25.40 1-month T-bills (0.46%) 22.40 6-month CDs (0.65%) 22.40 3-month T-bills (0.75%) 10.50 1-year CDs (1.25%) 24.50 5-year T-bonds (3.54%) 32.70 2-year CDs (2.35%) 21.70 4-year business loans (4.35%) 75.60 5-years CDs (4.42%) 61.30 8-year business loans, floating rate (5.38%, reset every quarter) 54.70 Long-term debt (5.67% fixed rate) 94.60 30-year mortgages, floating rate (4.25%, reset every 6 months) 76.30 Equity 30.20 Premises 4.50 Total Assets $ 280.10 Total Liabilities and Equity $ 280.10 a. Calculate the bank's net interest income (NII). (8 points) b. Calculate (1) the one-year repricing gap (CGAP) and (ii) the gap ratio for the bank. (6 points) c. Use the repricing gap model to estimate the change in net interest income (ANII) if interest rates are expected to increase by 250 basis points next year. Assume that the spread between rates on assets and liabilities remains constant. (3 points) d. Estimate All if interest rates on rate-sensitive assets increase by 2.25 basis points and interest rates on rate-sensitive liabilities increase 2.75 basis point. (4 points) e. Why are the answers in c. and d. different? How do these estimates represent the CGAP effect and the spread effect? Explain. (3 points) 3. Given the following balance sheet, analyze the bank's interest rate risk by answering the questions below. Dollars are in millions Assets Liabilities and Equity Cash $ 3.40 Demand deposits $ 25.40 1-month T-bills (0.46%) 22.40 6-month CDs (0.65%) 22.40 3-month T-bills (0.75%) 10.50 1-year CDs (1.25%) 24.50 5-year T-bonds (3.54%) 32.70 2-year CDs (2.35%) 21.70 4-year business loans (4.35%) 75.60 5-years CDs (4.42%) 61.30 8-year business loans, floating rate (5.38%, reset every quarter) 54.70 Long-term debt (5.67% fixed rate) 94.60 30-year mortgages, floating rate (4.25%, reset every 6 months) 76.30 Equity 30.20 Premises 4.50 Total Assets $ 280.10 Total Liabilities and Equity $ 280.10 a. Calculate the bank's net interest income (NII). (8 points) b. Calculate (1) the one-year repricing gap (CGAP) and (ii) the gap ratio for the bank. (6 points) c. Use the repricing gap model to estimate the change in net interest income (ANII) if interest rates are expected to increase by 250 basis points next year. Assume that the spread between rates on assets and liabilities remains constant. (3 points) d. Estimate All if interest rates on rate-sensitive assets increase by 2.25 basis points and interest rates on rate-sensitive liabilities increase 2.75 basis point. (4 points) e. Why are the answers in c. and d. different? How do these estimates represent the CGAP effect and the spread effect? Explain. (3 points)