Question

3. On 30 April 2021 a total amount of R34 000 was apportioned to the members from the profits of the CC. This amount was

3. On 30 April 2021 a total amount of R34 000 was apportioned to the members from the profits of the CC. This amount was paid in cash on this date.

4. The cash paid to the suppliers and employees for the 2021 financial year amounted to R300 990.

5. During the financial year Cavendish discontinued his membership and immigrated to Togo. Cavendish agreed that the CC repay his members contribution in 4 equal instalments. The balance of his members contribution account was closed off to a long-term loan account. The first instalment payment on the loan account was made on 31 January 2021.

6. The following transactions took place in respect of property, plant and equipment:

6.1 A vehicle was sold for cash during the financial year. At the date of the sale the carrying amount of this vehicle was R39 000. No other vehicles were bought or sold during the financial year.

6.2 Redundant equipment was written off during the financial year and replaced with new equipment which was purchased for cash at a cost of R18 300. No further equipment was sold or purchased during the financial year.

6.3 Additional buildings were constructed and paid for in cash.

QUESTION 1

Assume the correct cash receipts from customers is R500 000. Which of the following alternatives represents the correct amount that must be disclosed as cash generated from operations in the cash flows from operating activities section according to indirect method in the statement of cash flows of Matej CC for the year ended 30 April 2021?

A. 121 810

B. 199 010

C. 300 990

D. (300 990)

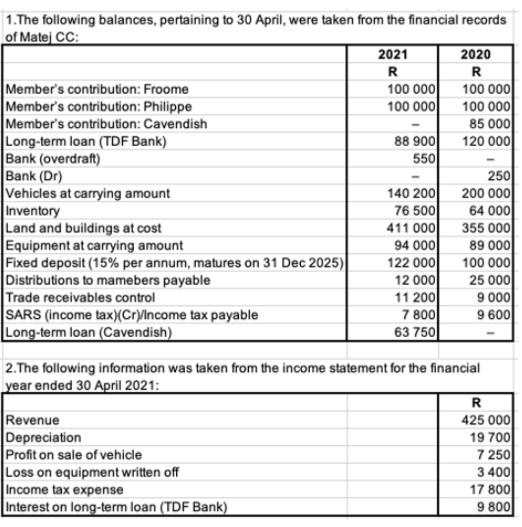

1. The following balances, pertaining to 30 April, were taken from the financial records of Mate CC: 2021 2020 R R Member's contribution: Froome 100 000 100 000 Member's contribution: Philippe 100 000 100 000 Member's contribution: Cavendish 85 000 Long-term loan (TDF Bank) 88 900 120 000 Bank (overdraft) 550 Bank (Dr) 250 Vehicles at carrying amount 140 2001 200 000 Inventory 76 5001 64 000 Land and buildings at cost 411 000 355 000 Equipment at carrying amount 94 000 89 000 Fixed deposit (15% per annum, matures on 31 Dec 2025) 122 0001 100 000 Distributions to mamebers payable 12 000 25 000 Trade receivables control 11 2001 9 000 SARS (income tax)(Cr)/Income tax payable 7 800 9 600 Long-term loan (Cavendish) 63 750 2. The following information was taken from the income statement for the financial year ended 30 April 2021: R Revenue 425 000 Depreciation 19 700 Profit on sale of vehicle 7 250 Loss on equipment written off 3 400 Income tax expense 17 800 Interest on long-term loan (TDF Bank) 9 800 1. The following balances, pertaining to 30 April, were taken from the financial records of Mate CC: 2021 2020 R R Member's contribution: Froome 100 000 100 000 Member's contribution: Philippe 100 000 100 000 Member's contribution: Cavendish 85 000 Long-term loan (TDF Bank) 88 900 120 000 Bank (overdraft) 550 Bank (Dr) 250 Vehicles at carrying amount 140 2001 200 000 Inventory 76 5001 64 000 Land and buildings at cost 411 000 355 000 Equipment at carrying amount 94 000 89 000 Fixed deposit (15% per annum, matures on 31 Dec 2025) 122 0001 100 000 Distributions to mamebers payable 12 000 25 000 Trade receivables control 11 2001 9 000 SARS (income tax)(Cr)/Income tax payable 7 800 9 600 Long-term loan (Cavendish) 63 750 2. The following information was taken from the income statement for the financial year ended 30 April 2021: R Revenue 425 000 Depreciation 19 700 Profit on sale of vehicle 7 250 Loss on equipment written off 3 400 Income tax expense 17 800 Interest on long-term loan (TDF Bank) 9 800Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rising From The Mailroom To The Boardroom Unique Insights For Governance Risk Compliance And Audit Leaders

Authors: Bruce Turner

1st Edition

1032042907, 978-1032042909