Answered step by step

Verified Expert Solution

Question

1 Approved Answer

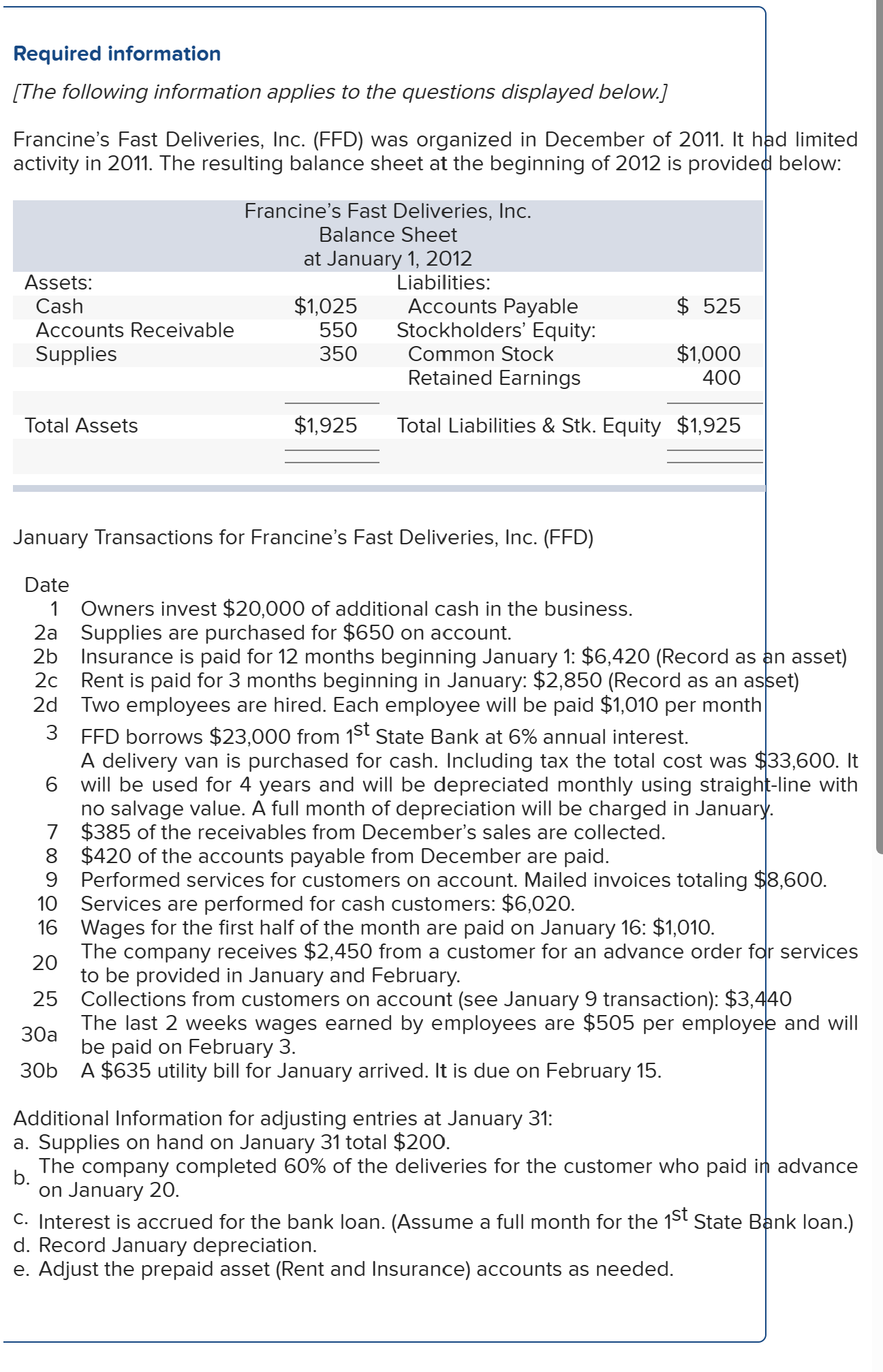

3. Prepare an unadjusted trial balance using the T-Account balances. Required information [The following information applies to the questions displayed below.] Francine's Fast Deliveries, Inc.

3.Prepare an unadjusted trial balance using the T-Account balances.

3.Prepare an unadjusted trial balance using the T-Account balances.

Required information [The following information applies to the questions displayed below.] Francine's Fast Deliveries, Inc. (FFD) was organized in December of 2011. It had limited activity in 2011. The resulting balance sheet at the beginning of 2012 is provided below: January Transactions for Francine's Fast Deliveries, Inc. (FFD) Date 1 Owners invest $20,000 of additional cash in the business. 2a Supplies are purchased for $650 on account. 2b Insurance is paid for 12 months beginning January 1: \$6,420 (Record as an asset) 2c Rent is paid for 3 months beginning in January: $2,850 (Record as an asset) 2d Two employees are hired. Each employee will be paid $1,010 per month 3 FFD borrows $23,000 from 1st State Bank at 6% annual interest. A delivery van is purchased for cash. Including tax the total cost was $33,600. It 6 will be used for 4 years and will be depreciated monthly using straight-line with no salvage value. A full month of depreciation will be charged in January. 7$385 of the receivables from December's sales are collected. 8$420 of the accounts payable from December are paid. 9 Performed services for customers on account. Mailed invoices totaling \$8,600. 10 Services are performed for cash customers: $6,020. 16 Wages for the first half of the month are paid on January 16 : $1,010. 20 The company receives $2,450 from a customer for an advance order for services to be provided in January and February. 25 Collections from customers on account (see January 9 transaction): $3,440 30 a The last 2 weeks wages earned by employees are $505 per employee and will be paid on February 3. 30b A \$635 utility bill for January arrived. It is due on February 15. Additional Information for adjusting entries at January 31: a. Supplies on hand on January 31 total $200. b. The company completed 60% of the deliveries for the customer who paid in advance on January 20. c. Interest is accrued for the bank loan. (Assume a full month for the 1st State Bank loan.) d. Record January depreciation. e. Adjust the prepaid asset (Rent and Insurance) accounts as needed

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Tools for business decision making

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

5th edition

470506954, 471345881, 978-0470506950, 9780471345886, 978-0470477144