Answered step by step

Verified Expert Solution

Question

1 Approved Answer

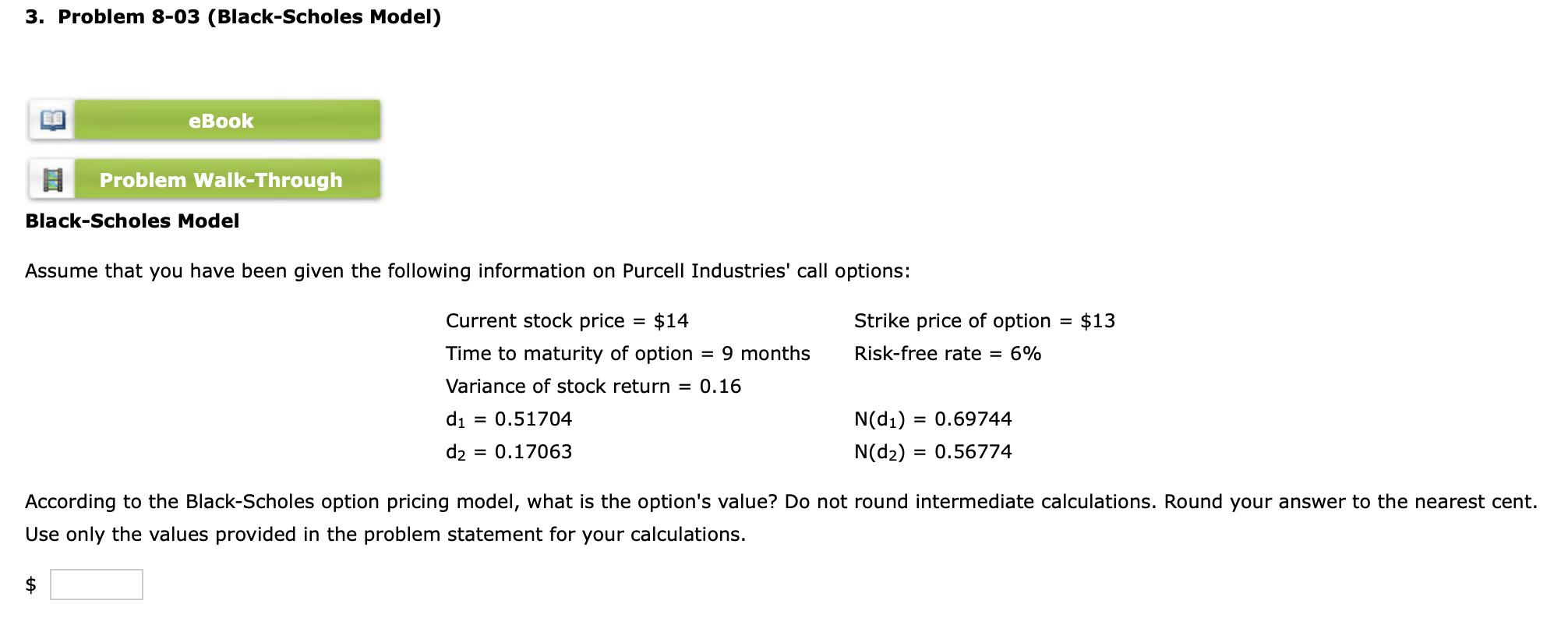

3. Problem 8-03 (Black-Scholes Model) Black-Scholes Model Assume that you have been given the following information on Purcell Industries' call options: Currentstockprice=$14Timetomaturityofoption=9monthsVarianceofstockreturn=0.16d1=0.51704d2=0.17063Strikepriceofoption=$13Risk-freerate=6%N(d1)=0.69744N(d2)=0.56774 According to the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Value Investing

Authors: Mike Hartley

1st Edition

979-8864443309