Answered step by step

Verified Expert Solution

Question

1 Approved Answer

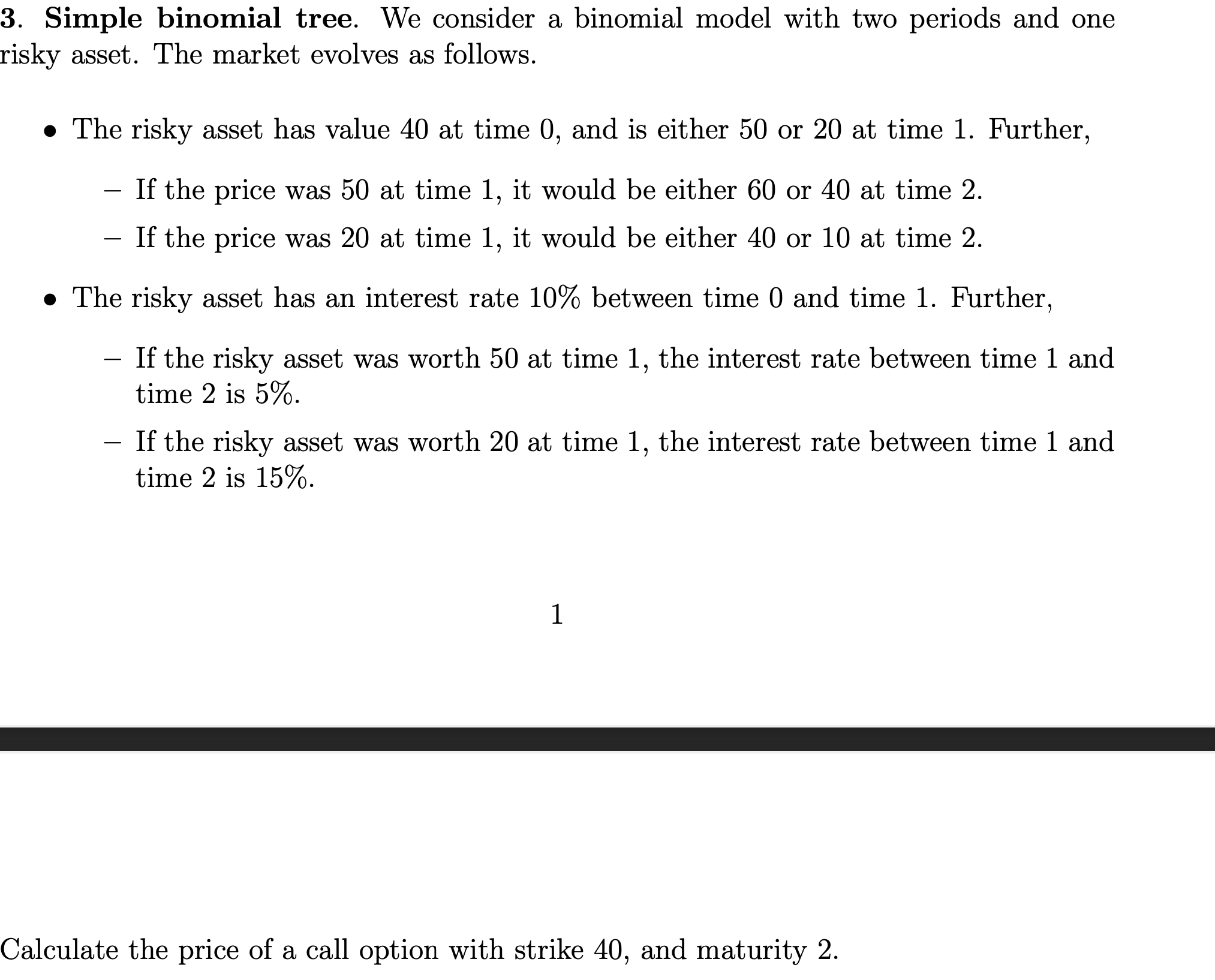

3. Simple binomial tree. We consider a binomial model with two periods and one risky asset. The market evolves as follows. The risky asset

3. Simple binomial tree. We consider a binomial model with two periods and one risky asset. The market evolves as follows. The risky asset has value 40 at time 0, and is either 50 or 20 at time 1. Further, - If the price was 50 at time 1, it would be either 60 or 40 at time 2. - If the price was 20 at time 1, it would be either 40 or 10 at time 2. The risky asset has an interest rate 10% between time 0 and time 1. Further, If the risky asset was worth 50 at time 1, the interest rate between time 1 and time 2 is 5%. If the risky asset was worth 20 at time 1, the interest rate between time 1 and time 2 is 15%. 1 Calculate the price of a call option with strike 40, and maturity 2.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus For Business, Economics And The Social And Life Sciences

Authors: Laurence Hoffmann, Gerald Bradley, David Sobecki, Michael Price

11th Brief Edition

978-0073532387, 007353238X