Answered step by step

Verified Expert Solution

Question

1 Approved Answer

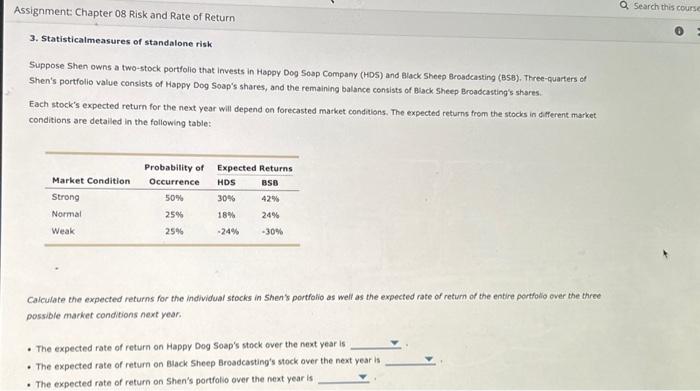

3. Statisticalmeasures of standalone risk Suppose Shen owns a two-stock portfolio that invests in Happy Dog Soap Company (HDS) and alack Sheep Brosdcasting (B5B). Three-quarters

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Hungary And Other Emerging EU Countries In The Financial Storm From Minor Turbulences To A Global Hurricane Financial And Monetary Policy Studies

Authors: Julia Kiraly

2020th Edition

3030495434, 978-3030495435