Answered step by step

Verified Expert Solution

Question

1 Approved Answer

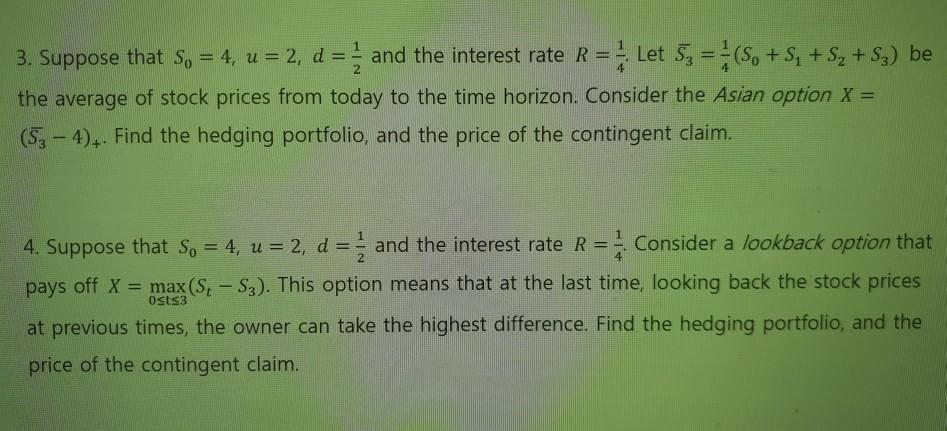

3. Suppose that So = 4, u = 2, d = and the interest rate R = Let 5= (S0+S + S + S3)

3. Suppose that So = 4, u = 2, d = and the interest rate R = Let 5= (S0+S + S + S3) be the average of stock prices from today to the time horizon. Consider the Asian option X = (S3-4). Find the hedging portfolio, and the price of the contingent claim. 4. Suppose that So = 4, u = 2, d = and the interest rate R = Consider a lookback option that pays off X= max (S, -S3). This option means that at the last time, looking back the stock prices 0sts3 at previous times, the owner can take the highest difference. Find the hedging portfolio, and the price of the contingent claim.

Step by Step Solution

★★★★★

3.46 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER 1 The american put has price VP 25...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516