Answered step by step

Verified Expert Solution

Question

1 Approved Answer

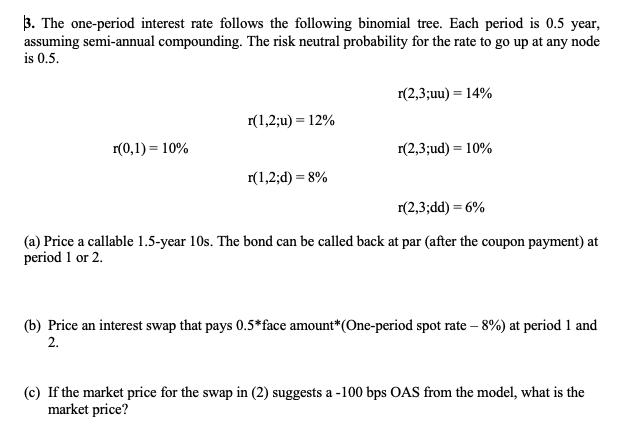

3. The one-period interest rate follows the following binomial tree. Each period is 0.5 year, assuming semi-annual compounding. The risk neutral probability for the

3. The one-period interest rate follows the following binomial tree. Each period is 0.5 year, assuming semi-annual compounding. The risk neutral probability for the rate to go up at any node is 0.5. r(0,1)= 10% r(1,2;u) = 12% r(1,2;d) = 8% r(2,3;uu) = 14% r(2,3;ud) = 10% r(2,3;dd) = 6% (a) Price a callable 1.5-year 10s. The bond can be called back at par (after the coupon payment) at period 1 or 2. (b) Price an interest swap that pays 0.5*face amount*(One-period spot rate - 8%) at period 1 and 2. (c) If the market price for the swap in (2) suggests a -100 bps OAS from the model, what is the market price?

Step by Step Solution

★★★★★

3.31 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

Answer 11 Given Data Binomial tree R01 Let t0 Current spot Price t 0 r 1212 r ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fixed Income Securities Valuation Risk and Risk Management

Authors: Pietro Veronesi

1st edition

0470109106, 978-0470109106