Answered step by step

Verified Expert Solution

Question

1 Approved Answer

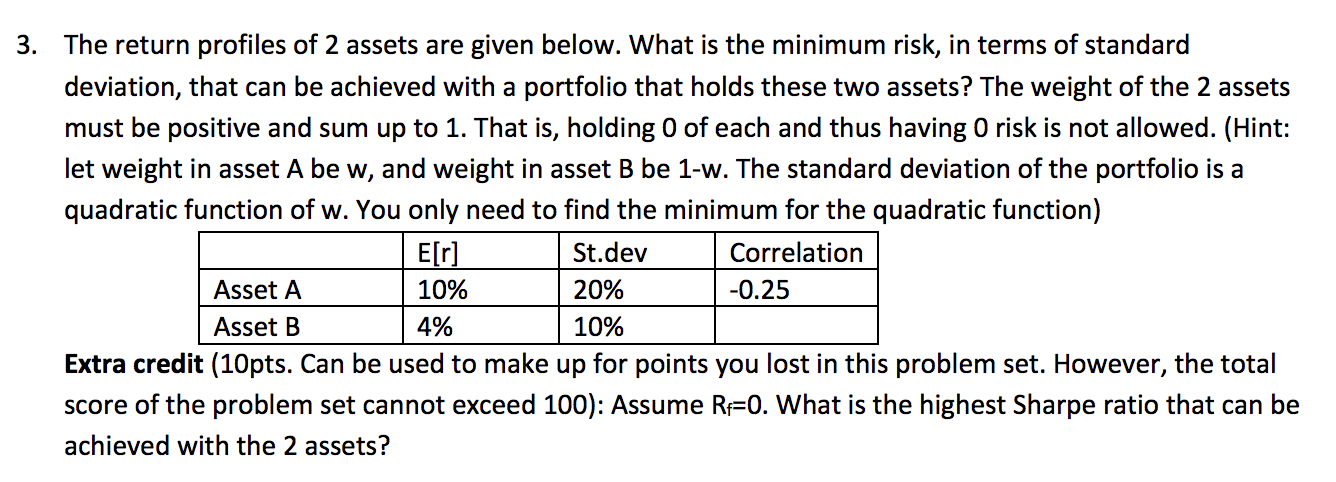

3. The return profiles of 2 assets are given below. What is the minimum risk, in terms of standard deviation, that can be achieved with

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Multinational Finance

Authors: Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman

5th edition

205989756, 978-0205989751