Answered step by step

Verified Expert Solution

Question

1 Approved Answer

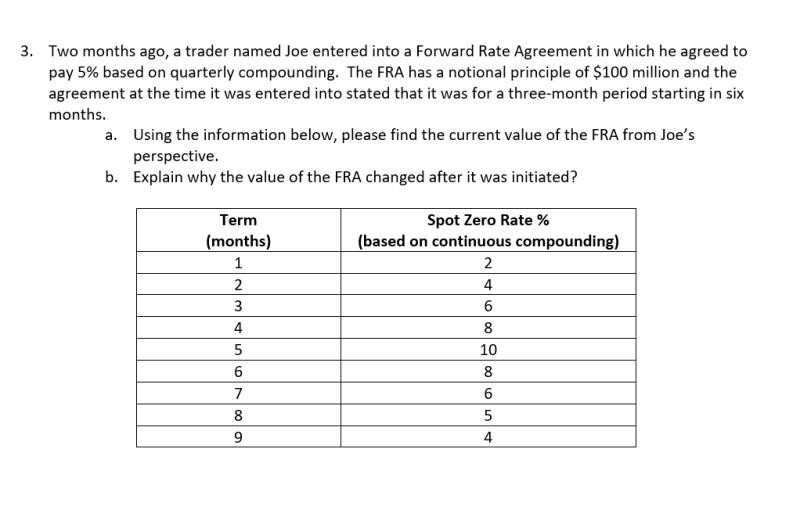

3. Two months ago, a trader named Joe entered into a Forward Rate Agreement in which he agreed to pay 5% based on quarterly compounding.

3. Two months ago, a trader named Joe entered into a Forward Rate Agreement in which he agreed to pay 5% based on quarterly compounding. The FRA has a notional principle of $100 million and the agreement at the time it was entered into stated that it was for a three-month period starting in six months. a. Using the information below, please find the current value of the FRA from Joe's perspective. b. Explain why the value of the FRA changed after it was initiated? Term (months) 1 2 3 4 5 6 7 8 9 Spot Zero Rate % (based on continuous compounding) 2 4 6 8 10 8 6 5 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Short Term Financial Management

Authors: Ned C. Hill, William L. Sartoris

3rd Edition

0023548320, 978-0023548321