Answered step by step

Verified Expert Solution

Question

1 Approved Answer

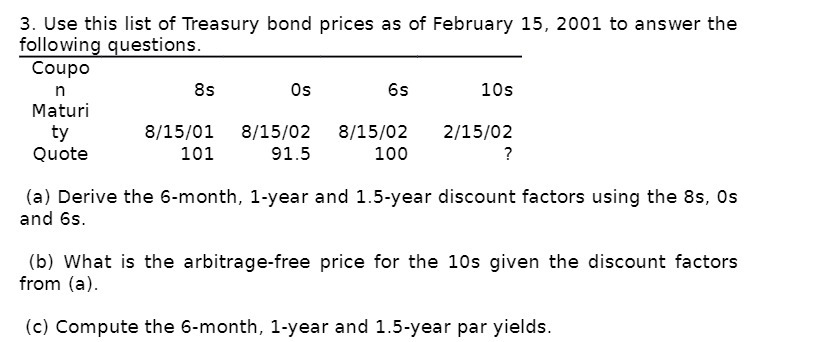

3. Use this list of Treasury bond prices as of February 15, 2001 to answer the following questions. Coupo n Maturi ty Quote 8s

3. Use this list of Treasury bond prices as of February 15, 2001 to answer the following questions. Coupo n Maturi ty Quote 8s Os 6s 8/15/01 8/15/02 8/15/02 101 91.5 100 10s 2/15/02 ? (a) Derive the 6-month, 1-year and 1.5-year discount factors using the 8s, Os and 6s. (b) What is the arbitrage-free price for the 10s given the discount factors from (a). (c) Compute the 6-month, 1-year and 1.5-year par yields.

Step by Step Solution

★★★★★

3.49 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

To answer the questions we need to calculate the discount factors and par yields based on the given Treasury bond prices Lets go step by step a Derivi...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Taxes And Business Strategy A Planning Approach

Authors: Myron Scholes, Mark Wolfson, Merle Erickson, Michelle Hanlon

5th Edition

132752670, 978-0132752671