Answered step by step

Verified Expert Solution

Question

1 Approved Answer

3. Working from case Exhibit 9, relative to the stand-alone value, estimate the dollar increase in DPC's value if a PE fund can obtain: a.

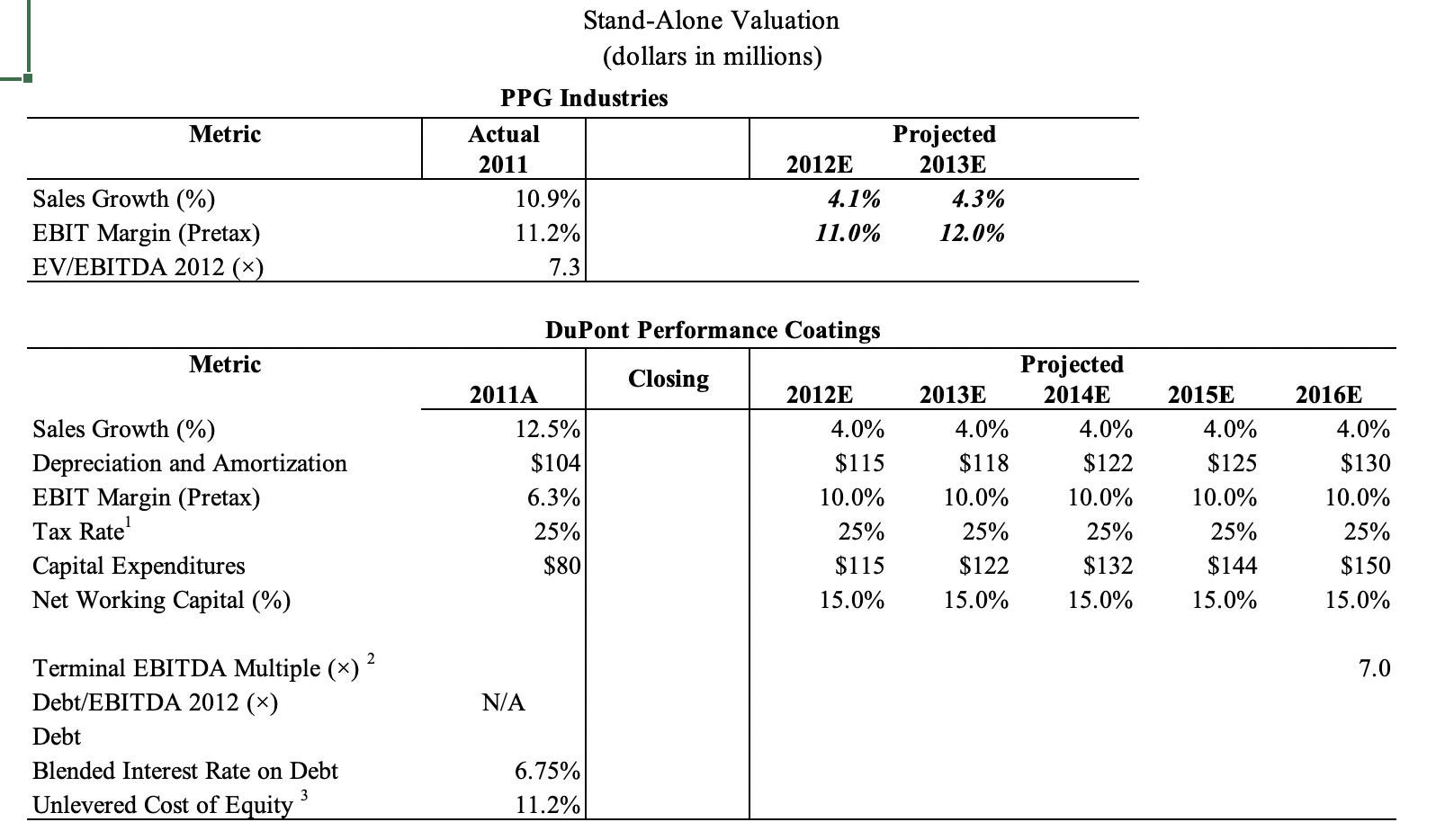

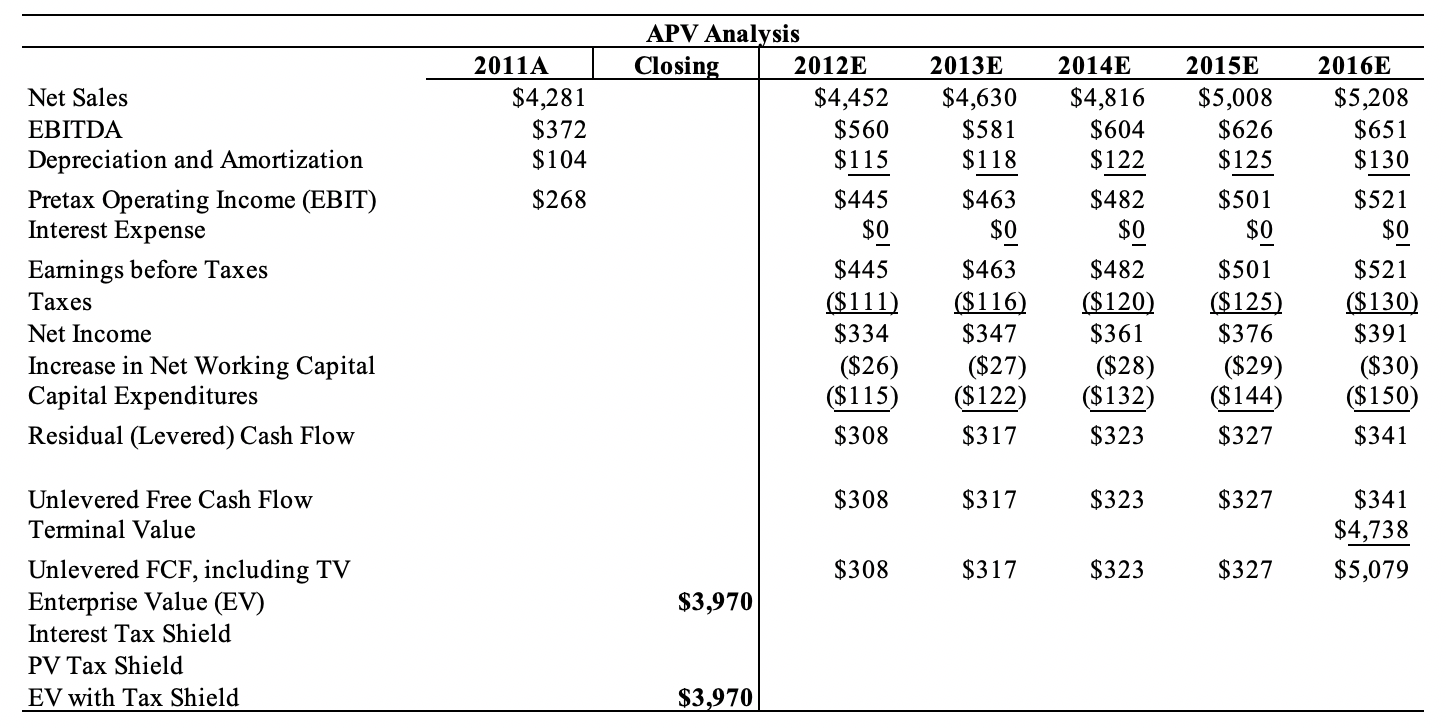

3. Working from case Exhibit 9, relative to the stand-alone value, estimate the dollar increase in DPC's value if a PE fund can obtain: a. 5% revenue growth per annum (versus 4% growth) in each of the next five years and improve the operating margin to 12% (versus 10%). b. Assume part a and that the division can be sold at 7.5x EBITDA in five years. c. Assume part a and part b and that debt financing equal to 6.0x forward EBITDA can be obtained. Assume that all cash available to pay debt each year (i.e., residual cash flow) is used to pay down the LBO debt and that, after five years, the firm will revert to an all-equity firm. Metric Stand-Alone Valuation (dollars in millions) PPG Industries Actual Projected 2011 2012E 2013E 10.9% 4.1% 4.3% 11.2% 11.0% 12.0% 7.3 Sales Growth (%) EBIT Margin (Pretax) EV/EBITDA 2012 (x) DuPont Performance Coatings Metric Closing Sales Growth (%) Depreciation and Amortization EBIT Margin (Pretax) Tax Rate Capital Expenditures Net Working Capital (%) 2011A 12.5% $104 6.3% 25% $80 2012E 4.0% $115 10.0% 25% $115 15.0% Projected 2013E 2014E 4.0% 4.0% $118 $122 10.0% 10.0% 25% 25% $122 $132 15.0% 15.0% 2015E 4.0% $125 10.0% 25% $144 2016E 4.0% $130 10.0% 25% $150 15.0% 15.0% 7.0 N/A Terminal EBITDA Multiple (x) ? Debt/EBITDA 2012 (*) Debt Blended Interest Rate on Debt Unlevered Cost of Equity" 6.75% 11.2% 2011A $4,281 $372 $104 APV Analysis Closing 2012E $4,452 $560 $115 2013E $4,630 $581 $118 2014E $4,816 $604 $122 2015E $5,008 $626 $125 2016E $5,208 $651 $130 $268 $445 $0 $463 $0 $482 $0 $501 $0 $521 $0 Net Sales EBITDA Depreciation and Amortization Pretax Operating Income (EBIT) Interest Expense Earnings before Taxes Taxes Net Income Increase in Net Working Capital Capital Expenditures Residual (Levered) Cash Flow $445 ($111) $334 ($26) ($115) $308 $463 ($116) $347 ($27) ($122) $317 $482 ($120) $361 ($28) ($132) $323 $501 ($125) $376 ($29) ($144) $327 $521 ($130) $391 ($30) ($150) $341 $308 $317 $323 $327 $341 $4,738 $5,079 $308 $317 $323 $327 Unlevered Free Cash Flow Terminal Value Unlevered FCF, including TV Enterprise Value (EV) Interest Tax Shield PV Tax Shield EV with Tax Shield $3,970 $3,970 Data sources: Historical information for DPC is from DuPont company Databooks. Projections are case writer estimates. PPG's enterprise value is based on prices at the end of January 2012. PPG's projections are based on Buckingham Research Group analyst report, PPG Industries: "Other Industrial Coatings Review, May 21, 2012. Notes to stand-alone model: 1 DPC's estimated average tax rate of 25% is lower than the U.S. marginal corporate tax rate as a result of international operations taxed at lower rates. 2 Assumed forward exit multiple for Terminal Value is based on projected EBITDA growth in 2017 and is below PPG's multiple because of lower margins and slightly lower growth. 3 Unlevered Cost of Equity (ku) is based on PPG's estimated unlevered beta of 1.2, a normalized 4% long-term U.S. Treasury rate, and a 6% market risk premium. 3. Working from case Exhibit 9, relative to the stand-alone value, estimate the dollar increase in DPC's value if a PE fund can obtain: a. 5% revenue growth per annum (versus 4% growth) in each of the next five years and improve the operating margin to 12% (versus 10%). b. Assume part a and that the division can be sold at 7.5x EBITDA in five years. c. Assume part a and part b and that debt financing equal to 6.0x forward EBITDA can be obtained. Assume that all cash available to pay debt each year (i.e., residual cash flow) is used to pay down the LBO debt and that, after five years, the firm will revert to an all-equity firm. Metric Stand-Alone Valuation (dollars in millions) PPG Industries Actual Projected 2011 2012E 2013E 10.9% 4.1% 4.3% 11.2% 11.0% 12.0% 7.3 Sales Growth (%) EBIT Margin (Pretax) EV/EBITDA 2012 (x) DuPont Performance Coatings Metric Closing Sales Growth (%) Depreciation and Amortization EBIT Margin (Pretax) Tax Rate Capital Expenditures Net Working Capital (%) 2011A 12.5% $104 6.3% 25% $80 2012E 4.0% $115 10.0% 25% $115 15.0% Projected 2013E 2014E 4.0% 4.0% $118 $122 10.0% 10.0% 25% 25% $122 $132 15.0% 15.0% 2015E 4.0% $125 10.0% 25% $144 2016E 4.0% $130 10.0% 25% $150 15.0% 15.0% 7.0 N/A Terminal EBITDA Multiple (x) ? Debt/EBITDA 2012 (*) Debt Blended Interest Rate on Debt Unlevered Cost of Equity" 6.75% 11.2% 2011A $4,281 $372 $104 APV Analysis Closing 2012E $4,452 $560 $115 2013E $4,630 $581 $118 2014E $4,816 $604 $122 2015E $5,008 $626 $125 2016E $5,208 $651 $130 $268 $445 $0 $463 $0 $482 $0 $501 $0 $521 $0 Net Sales EBITDA Depreciation and Amortization Pretax Operating Income (EBIT) Interest Expense Earnings before Taxes Taxes Net Income Increase in Net Working Capital Capital Expenditures Residual (Levered) Cash Flow $445 ($111) $334 ($26) ($115) $308 $463 ($116) $347 ($27) ($122) $317 $482 ($120) $361 ($28) ($132) $323 $501 ($125) $376 ($29) ($144) $327 $521 ($130) $391 ($30) ($150) $341 $308 $317 $323 $327 $341 $4,738 $5,079 $308 $317 $323 $327 Unlevered Free Cash Flow Terminal Value Unlevered FCF, including TV Enterprise Value (EV) Interest Tax Shield PV Tax Shield EV with Tax Shield $3,970 $3,970 Data sources: Historical information for DPC is from DuPont company Databooks. Projections are case writer estimates. PPG's enterprise value is based on prices at the end of January 2012. PPG's projections are based on Buckingham Research Group analyst report, PPG Industries: "Other Industrial Coatings Review, May 21, 2012. Notes to stand-alone model: 1 DPC's estimated average tax rate of 25% is lower than the U.S. marginal corporate tax rate as a result of international operations taxed at lower rates. 2 Assumed forward exit multiple for Terminal Value is based on projected EBITDA growth in 2017 and is below PPG's multiple because of lower margins and slightly lower growth. 3 Unlevered Cost of Equity (ku) is based on PPG's estimated unlevered beta of 1.2, a normalized 4% long-term U.S. Treasury rate, and a 6% market risk premium

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Megan Noel, Dan French

2nd Edition

1465246479, 9781465246479