Answered step by step

Verified Expert Solution

Question

1 Approved Answer

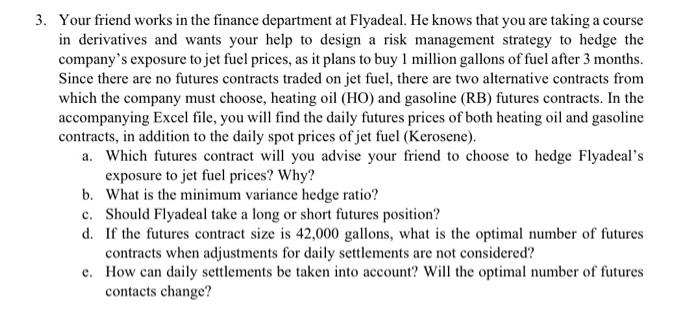

3. Your friend works in the finance department at Flyadeal. He knows that you are taking a course in derivatives and wants your help to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Conflict Resolution

Authors: Oliver Ramsbotham, Tom Woodhouse, Hugh Miall

3rd Edition

0745649742,1509509542