Question

CONTINUING CASE Investing Fundamentals The triplets are now three and a half years old and Jamie Lee and Ross, both 38, are finally beginning to

CONTINUING CASE

Investing Fundamentals

The triplets are now three and a half years old and Jamie Lee and Ross, both 38, are finally beginning to settle into a regular routine now that the triplets are a little more self-sufficient. The first three years were a blur of diapers, feedings,

baths, mounds of laundry, and crying babies! Jamie Lee and Ross finally had a welcomed dinner out on their own as Rosss parents were minding the triplets. They were having a conversation about their future and the future of the triplets. College expenses ($100,000) and their eventual retirement seem to be a major worry of both of them. They both have dreamed of owning a beach house when they retire. That could be another $350,000, thirty years from now. They wondered how they could possibly afford all of this.

They agreed that it was time to talk to an investment counselor but wanted to organize all of their financial information and discuss their familys financial goals before setting up the appointment.

Current Financial Situation

Assets (Jamie Lee and Ross combined):

Checking account: $4,500

Savings account: $20,000

Emergency fund savings account: $21,000

IRA balance: $32,000

Car: $8,500 (Jamie Lee) and $14,000 (Ross)

Liabilities (Jamie Lee and Ross combined):

Student loan balance: $0

Credit card balance: $4,000

Car loans: $2,000

Income:

Jamie Lee: $45,000 gross income ($31,500 net income after taxes)

Ross: $80,000 gross income ($64,500 net income after taxes)

Monthly Expenses:

Mortgage: $1,225

Property taxes: $400

Homeowners insurance: $200

IRA contribution $300

Utilities: $250

Food: $600

Baby essentials (diapers, clothing, toys, etc.): $200

Gas/maintenance: $275

Credit card payment: $400

Car loan payment: $289

Entertainment: $125

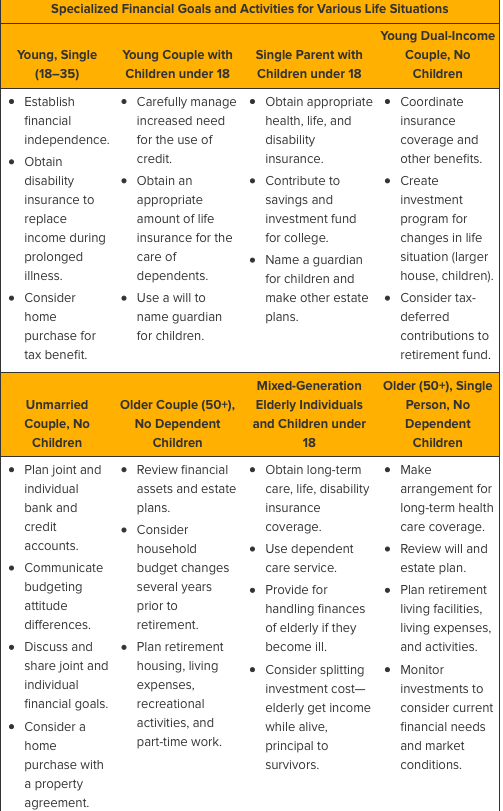

- Looking back to Chapter 1 and Exhibit 1-6, Financial goals and activities for various life situations, describe the life stage that corresponds with what Jamie Lee and Ross are experiencing right now. What are some of the financial activities that they should be participating in?

- After reviewing Jamie Lee and Rosss current financial situation, suggest specific and measurable short-term and long-term financial goals they can implement at this stage.

- Access the validity of Jamie Lee and Rosss Short- and long-term financial goals and objectives.

| Financial Question | Short-term Goals | Long-Term Goals |

| How much money do they need to satisfy their investment goals? |

|

|

| How will they obtain the money? |

|

|

| How long will it take them to obtain the money? |

|

|

| How much risk are they willing to assume in an investment program? |

|

|

| What possible economic or personal conditions could alter their investment goals? |

|

|

| Considering current Economic conditions, are their investment goals reasonable? |

|

|

| Are they willing to make the sacrifices necessary to ensure that they meet their investment goals? |

|

|

4. Using the formula determining the amount of growth investments investors should have, how much of Jamie Lee and Rosss assets should be allocated in growth investments? How should the remaining investments be distributed and what is the associated risk with each type of investment?

5. Jamie Lee and Ross need to evaluate their emergency fund of $21,000 will their present emergency fund be sufficient to cover them should one of them lose their job?

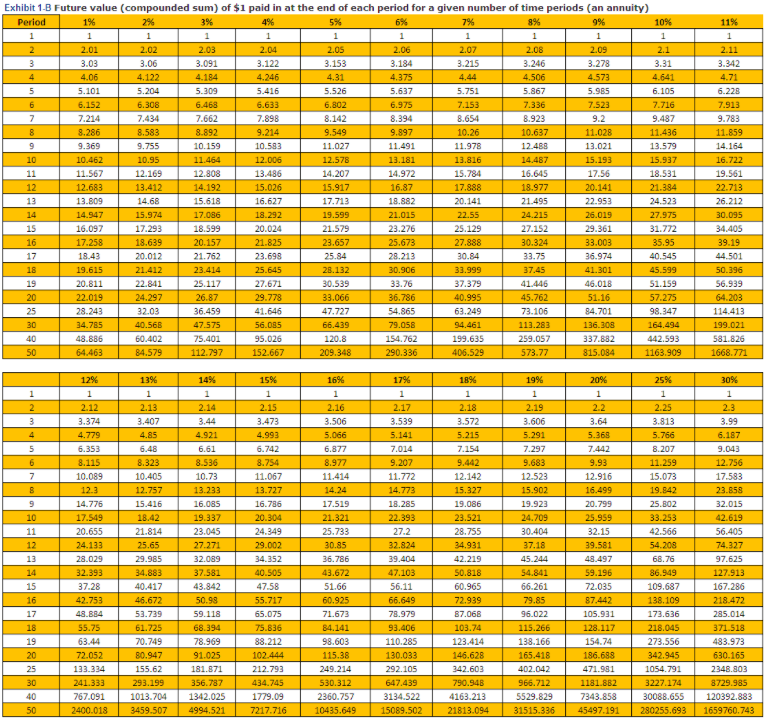

6. Jamie Lee and Ross agree that by accomplishing their short-term goals, they can budget $5,000 a year toward their long-term investment goals. They are estimating that with the allocations recommended by their financial adviser, that they will see an average return of 7 percent on their investments. The triplets will begin college in 15 years and will need $100,000 for tuition. Using Exhibit 1-B, Future Value in the Time Value of Money Appendix located after chapter 1, decide whether Jamie Lee and Ross will be on track to reaching their long-term financial goals of having enough money from their investments to pay the triplets tuition.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Conflict Resolution

Authors: Oliver Ramsbotham, Tom Woodhouse, Hugh Miall

3rd Edition

0745649742,1509509542