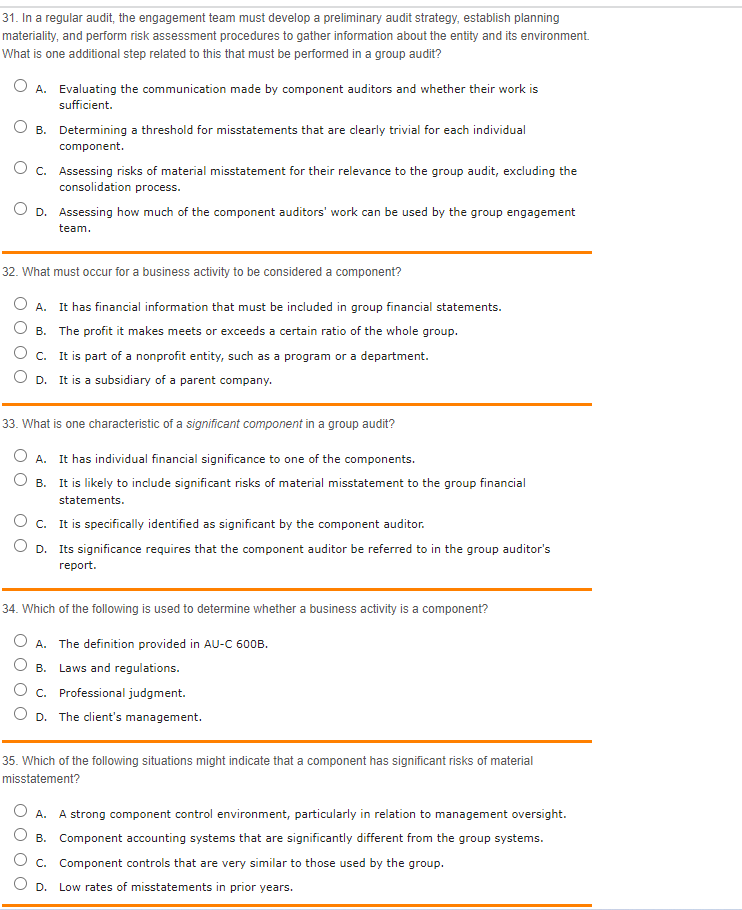

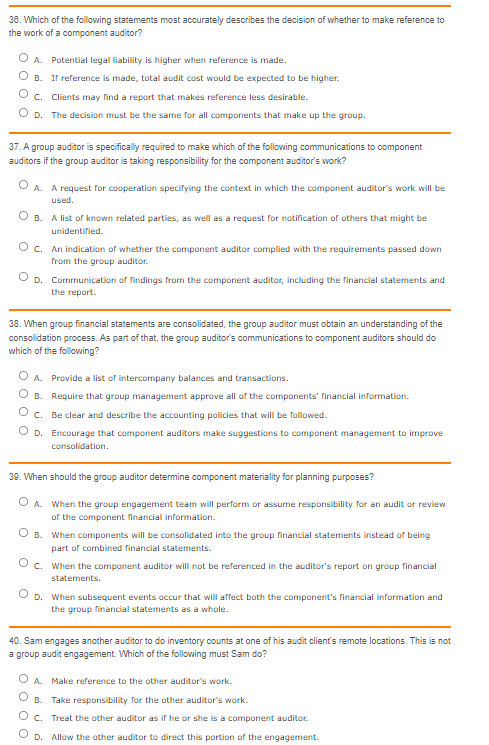

31. In a regular audit, the engagement team must develop a preliminary audit strategy, establish planning materiality, and perform risk assessment procedures to gather information about the entity and its environment. What is one additional step related to this that must be performed in a group audit? O A. Evaluating the communication made by component auditors and whether their work is sufficient. O B. Determining a threshold for misstatements that are clearly trivial for each individual component. O c. Assessing risks of material misstatement for their relevance to the group audit, excluding the consolidation process. D. Assessing how much of the component auditors' work can be used by the group engagement team. 32. What must occur for a business activity to be considered a component? O A. It has financial information that must be included in group financial statements. B. The profit it makes meets or exceeds a certain ratio of the whole group. O c. It is part of a nonprofit entity, such as a program or a department. OD. It is a subsidiary of a parent company. 33. What is one characteristic of a significant component in a group audit? O A. It has individual financial significance to one of the components. OB. It is likely to include significant risks of material misstatement to the group financial statements. O c. It is specifically identified as significant by the component auditor. OD. Its significance requires that the component auditor be referred to in the group auditor's report. 34. Which of the following is used to determine whether a business activity is a component? O A. The definition provided in AU-C 600B. . Laws and regulations. O c. Professional judgment. D. The client's management. 35. Which of the following situations might indicate that a component has significant risks of material misstatement? O A. A strong component control environment, particularly in relation to management oversight. B. Component accounting systems that are significantly different from the group systems. O c. Component controls that are very similar to those used by the group. OD. Low rates of misstatements in prior years. 38. Which of the following statements most accurately describes the decision of whether to make reference to the work of a component auditor? O A. Potential legal liability is higher when reference is made. O B. If reference is made, total audit cost would be expected to be higher. O c. Clients may find a report that makes reference less desirable. OD. The decision must be the same for all components that make up the group. 37. A group auditor is specifically required to make which of the following communications to component auditors if the group auditor is taking responsibility for the component auditor's work? O A. A request for cooperation specifying the context in which the component auditor's work will be used. OB. A list of known related parties, as well as a request for notification of others that might be unidentified. O c. An indication of whether the component auditor complied with the requirements passed down from the group auditor. O D. Communication of findings from the component auditor, including the financial statements and the report. 38. When group financial statements are consolidated the group auditor must obtain an understanding of the consolidation process. As part of that, the group auditor's communications to component auditors should do which of the following? O A. Provide a list of intercompany balances and transactions. O B. Require that group management approve all of the components' financial information. O c. Be clear and describe the accounting policies that will be followed. OD. Encourage that component auditors make suggestions to component management to improve consolidation. 39. When should the group auditor determine component materiality for planning purposes? O A. When the group engagement team will perform or assume responsibility for an audit or review of the component financial information. O B. When components will be consolidated into the group financial statements instead of being part of combined financial statements. O c. When the component auditor will not be referenced in the auditor's report on group financial statements. D. When subsequent events occur that will affect both the component's financial information and the group financial statements as a whole. 40. Sam engages another auditor to do inventory counts at one of his audit client's remote locations. This is not a group audit engagement. Which of the following must Sam do? OA Make reference to the other auditor's work. B. Take responsibility for the other auditor's work. O C. Treat the other auditor as if he or she is a component auditor. D. Allow the other auditor to direct this portion of the engagement